Interpretation of Core Data

The November production data clearly reflects an overall industry pattern of “pressure at the top, divergence at the bottom.” The sector has entered an adjustment phase, with most companies reporting flat or declining production volumes month-on-month (MoM). In November, the total output of the TOP20 PV module manufacturers was approximately 39.29 GW, a decrease of 7.73% MoM, indicating a continued weakening of end-market demand.

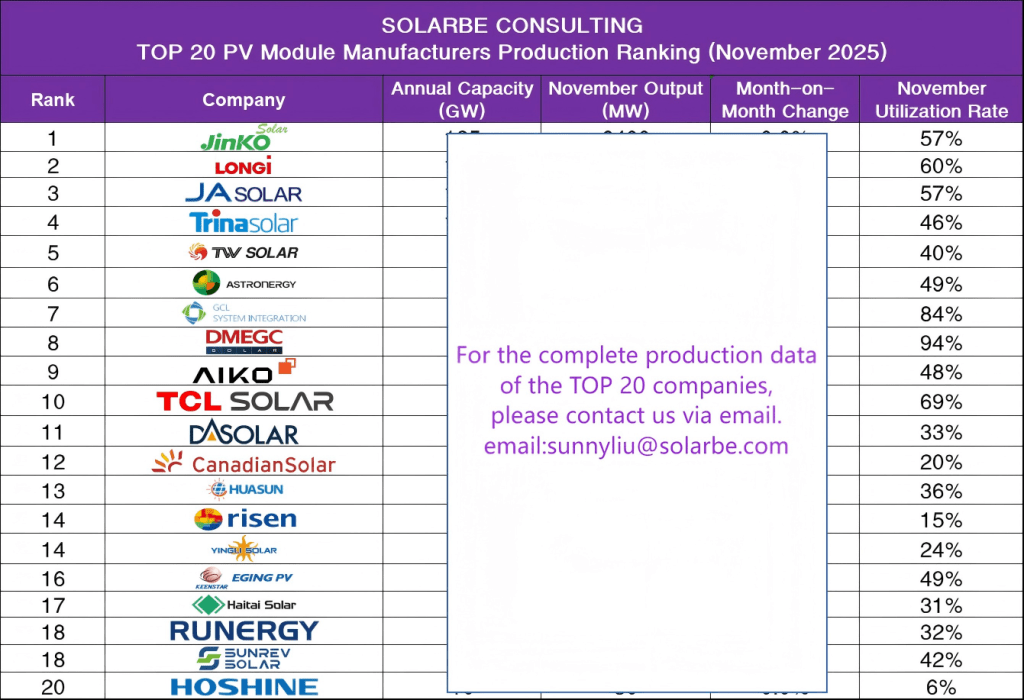

Intensifying Polarization Among Enterprises

Leading firms maintain stable market share but face widespread pressure: The combined output of the top five manufacturers—Jinko, LONGi, JA Solar, Trina Solar, and Tongwei—accounted for 62.6% of the TOP 20 total, demonstrating extremely high market concentration. However, with the exception of Jinko, the other four leading companies all experienced a MoM decline in November output. Their operating rates were generally below 60%, reflecting a market strategy of trading price for volume and pressure to reduce inventory.

Tail-end enterprises face severe survival tests with divergent strategies: Companies ranked lower show two distinct survival states. Some, like GCL and DMEGC, have achieved operating rates (84% and 94%, respectively) far exceeding the industry average by leveraging specific technological pathways or market strategies. Others, like Hoshine Silicon Industry with a mere 6% operating rate, and companies like Risen, Yingli, and Canadian Solar with rates below 30%, suffer from extremely low capacity utilization and face significant operational pressure.

Trend Forecast for Q1 2026

Continued contraction in output and production schedules: Enterprises currently face inventory pressure and low order visibility. Data shows that module production schedules for December 2025 are set to decline sharply. This strategy of proactive production cuts and producing to order is likely to continue into the first quarter of 2026 to alleviate supply-demand imbalance.

Accelerated capacity exit and industry consolidation: Under prolonged pressure from price inversions and losses, outdated capacity and uncompetitive firms will accelerate their exit. The industry consensus has shifted from expanding scale to “reducing output” and “exiting capacity.” An increase in mergers and acquisitions is anticipated.

Policy and market demand seeking new equilibrium: Domestically, the effects of the new “Document No. 136” policy, which impacts project returns, will continue to be felt. The market needs time to digest and adapt to the new electricity pricing mechanism. Overseas markets also face challenges, with demand likely to remain subdued in the short term. Growth momentum will rely more on domestic large-scale base projects, green power consumption responsibility mechanisms, and other policy-driven certainties.

{kind=link}