By mid-November, the EU carbon price had exceeded €80 per ton, continuing its upward trend since late August. This rise has been driven mainly by robust investment fund activity and market expectations of tightening allowance supply in the coming years.

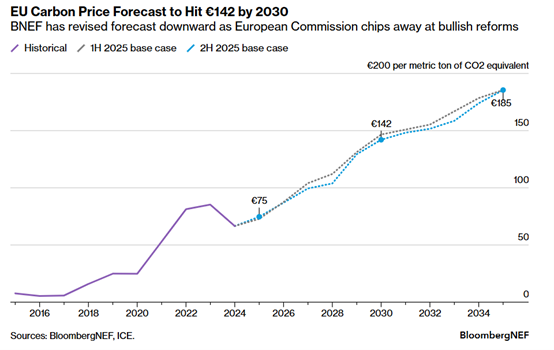

BloombergNEF (BNEF) forecasts that if current policies remain unchanged, the average price of EU Allowances (EUA) will reach €75 per ton by the end of 2025. Between 2025 and 2030, European carbon prices could increase by 90%, potentially reaching €142 per ton by 2030 and €185 per ton by 2035.

The chart illustrates BNEF’s latest projections for EU carbon prices: from €75 per ton in 2025, prices are expected to surge to €142 per ton by 2030 and rise further to €185 per ton by 2035, with the possibility of exceeding €200 per ton.

As the EU navigates the delicate balance between advancing decarbonization efforts and maintaining industrial competitiveness, future changes to market rules are possible.

Carbon allowance supply comes from free allocation and auctions. Each year, the European Commission allocates free allowances to industries facing competition from regions with no or low carbon pricing to provide support, while the remaining allowances are sold through auctions on the European Energy Exchange (EEX).

According to BNEF data, under the EU Emissions Trading System (EU ETS) — the world’s largest cap-and-trade program — free allocations are projected to decline from the current 499 million tons to 121 million tons of CO₂ (MtCO₂) by 2035. This reduction is driven primarily by the gradual phase-out of free allowances due to the progressive implementation of the Carbon Border Adjustment Mechanism (CBAM), a carbon tariff on imported goods designed to level the playing field for European companies. Additionally, updates to industry benchmarks between 2026 and 2030 will further reduce the volume of free allowances.

Auctioned allowances are also expected to decrease, dropping from 589 million tons of CO₂ in 2025 to 294 million tons of CO₂ by 2035, reflecting the continued tightening of the EU ETS cap. In 2026, auction supply could fall by 27%, largely due to the delayed cancellation of surplus allowances from the shipping sector, which will reduce supply by 54 million tons of CO₂.

The auction volumes earmarked for the REPowerEU initiative — aimed at raising funds to reduce dependence on Russian fossil fuels — may also decline in 2026, as monetary targets could be met earlier than anticipated if carbon prices remain high.

This tightening trajectory could reduce total supply by 26% between 2025 and 2030, pushing EU carbon prices to €142 per ton by 2030, marking the end of Phase IV of the EU ETS. Although details of the market design beyond this phase remain uncertain, BNEF projects that prices could reach €185 per ton by 2035 if current policy parameters remain unchanged.

As carbon costs rise and low-cost emission reduction opportunities begin to diminish, higher carbon prices will incentivize the adoption of low-carbon industrial solutions such as carbon capture, utilization, and storage (CCUS). This could accelerate the decarbonization of hard-to-abate sectors like steel and cement.

{kind=link}