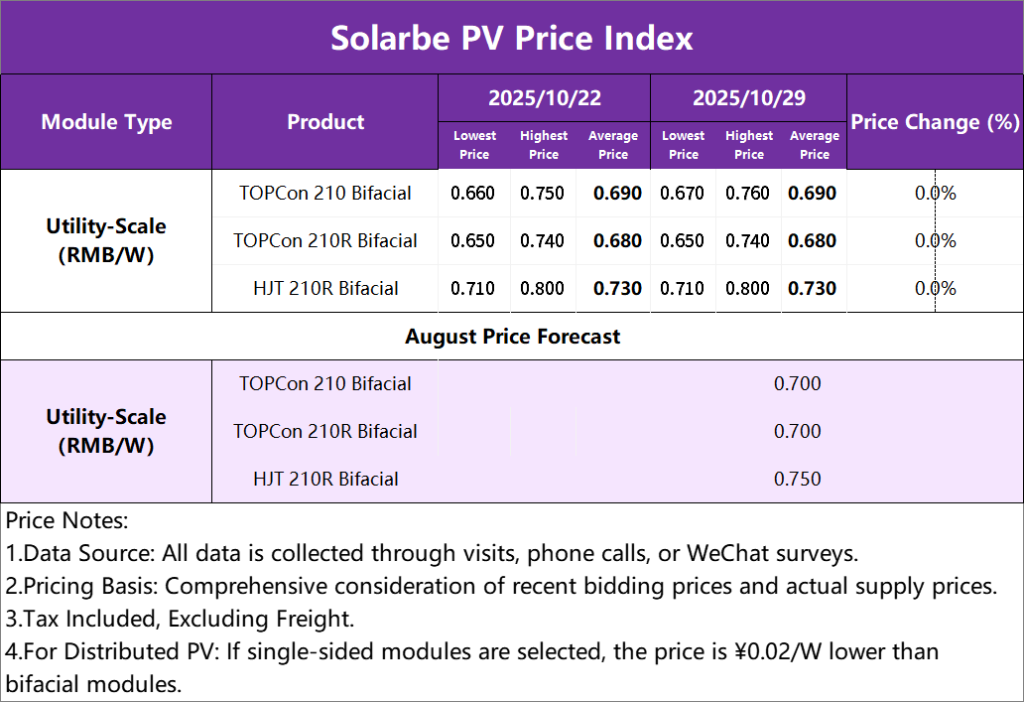

Photovoltaic Modules

Module prices remained unchanged this week. For ground-mounted power stations, the price for TOPCon 210 bifacial modules was 0.690 yuan/W, for TOPCon rectangular bifacial modules was 0.680 yuan/W, and for HJT rectangular bifacial modules was 0.730 yuan/W.

In terms of supply and demand, the production reduction plans of upstream polysilicon and wafer companies in November are the most significant positive factors in the current market, helping to alleviate supply pressure across the entire industry chain. Market expectations for terminal module demand in the fourth quarter remain pessimistic. Centralized projects are primarily executing previous orders, with limited visibility on new orders, and the distributed market has not shown strong recovery signals.

Regarding installations, according to the national power industry statistics for January-September 2025 released by the National Energy Administration, newly added PV installed capacity in September was 9.66 GW, a month-on-month increase of 31.25% compared to 7.36 GW in August, but a year-on-year decrease of 53.76% compared to 20.89 GW in the same period last year. The cumulative newly added PV installed capacity in the first three quarters was 240.27 GW, a year-on-year increase of 49.35%, showing an overall trend of high growth in the first half and lower growth in the second half.

In terms of prices, although there is an expectation for polysilicon prices to decrease, all segments of the industry chain are still facing significant cost pressures, leaving very limited room for module manufacturers to further reduce prices. Based on a comprehensive assessment of various current market factors, PV module prices are expected to remain generally stable in the short term, but face significant upward resistance. It cannot be ruled out that some products may face pressure due to weak demand. High-power modules (700W+) are expected to maintain firm prices, driven primarily by demand from domestic centralized projects and their own low inventory levels. Conventional power module prices will continue to be under pressure, representing the main area of price pressure in the market. If terminal demand does not improve significantly, inventory reduction pressures may cause their prices to fluctuate at the current low levels.

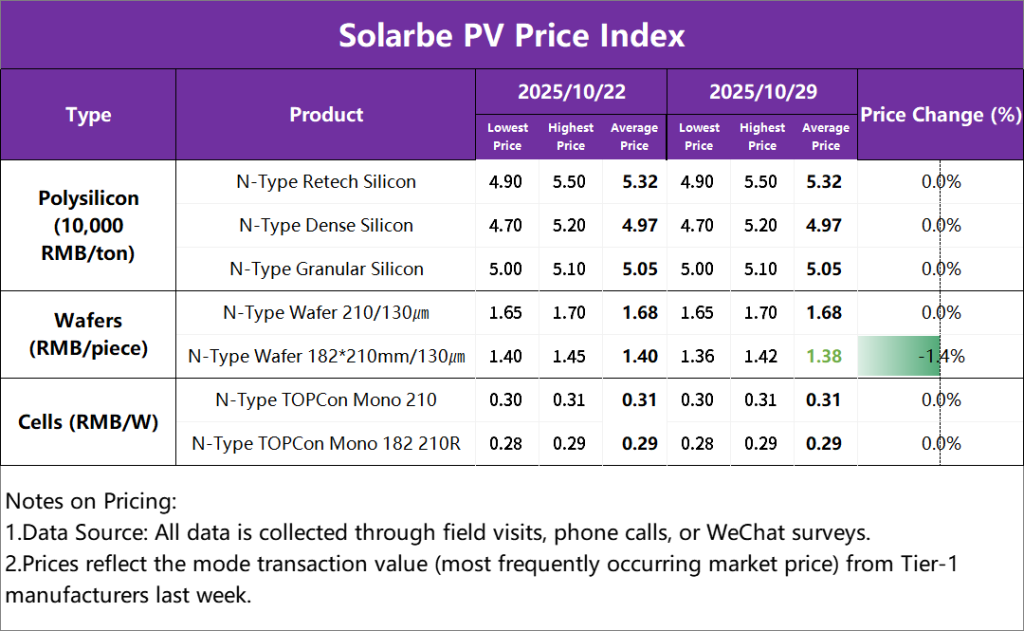

Polysilicon/Wafers/Cells

Polysilicon prices remained unchanged this week. The average price for N-type recycled materials was 53,200 yuan/ton, for N-type dense materials was 49,700 yuan/ton, and for N-type granular silicon was 50,500 yuan/ton.

In terms of supply and demand, data from the Silicon Industry Branch indicates that polysilicon production in the fourth quarter is expected to be about 382,000 tons, a year-on-year increase of 3.0%. Several major polysilicon producers plan to halt production in November, and overall output is expected to decrease. Total industry inventory is approximately over 420,000 tons and shows a trend of continued accumulation. Terminal demand is weak, downstream wafer companies are maintaining stable operating rates, and polysilicon procurement demand is generally stable with a cautious strategy. Polysilicon prices are expected to remain stable in the short term, but the characteristic of having prices without a vibrant market is likely to become more pronounced.

Wafer prices decreased this week. The average price for N-type 210 wafers was 1.68 yuan/piece, and for N-type 182*210mm wafers was 1.38 yuan/piece. Regarding supply and demand, based on production schedules, wafer companies are basically confirmed to implement production reductions in November-December. This will help alleviate market supply pressure and provide a bottom support for prices. Upstream polysilicon prices are currently stable, and the firmness on the cost side makes wafer companies reluctant to significantly reduce prices. The wafer market is currently in a stalemate under a weak supply-demand balance. The price trend is highly dependent on the actual launch pace of centralized projects in the fourth quarter and the actual implementation effect of the November production reduction plans.

Cell prices remained unchanged this week. The average price for N-type TOPCon monocrystalline 210 cells was 0.31 yuan/W, and for N-type TOPCon monocrystalline 210R cells was 0.29 yuan/W. In terms of supply and demand, market expectations for PV installations in the fourth quarter are generally weak, and order increments for cells are limited. Inventory structures in the cell segment are diverging; 210R and 183 models still face certain inventory pressures. 210 cell prices are expected to remain firm and may even strengthen slightly due to demand support.

{kind=link}