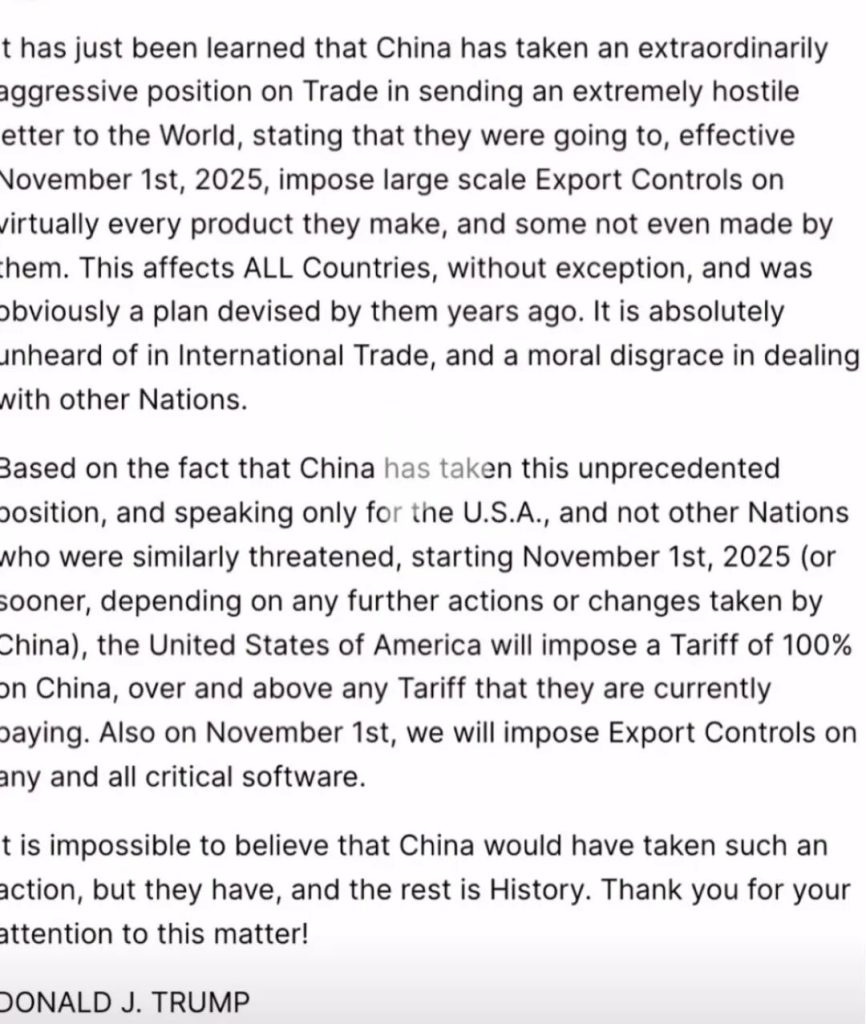

On October 10, 2025, former US President Donald Trump announced a plan to impose an additional 100% tariff on all Chinese imports effective November 1, 2025 . Combined with existing tariffs, the actual tax rate would surge significantly. He also declared that export controls would be implemented on all critical software simultaneously .

In his statement, Trump claimed that “China has taken an unprecedented stance” and indicated that the timing for imposing the additional tariffs might be moved up depending on China’s subsequent actions . This policy poses severe challenges to China’s foreign trade sector, particularly the photovoltaic (PV) industry.

According to previous disclosures from the Fuxin Municipal Government, the US had already increased tariffs on solar cells and modules from 25% to 50% effective August 1, 2025. The proposed additional 100% tariff would double the tax burden on these products again. Although direct exports of Chinese PV modules to the US accounted for only 0.77% of total exports in 2024 , the US market supply heavily relies on production capacity布局 (bùjú, layout) by Chinese companies in Southeast Asia. However, since 2022, anti-circumvention investigations targeting four Southeast Asian countries have significantly weakened their role as a “stepping stone” .

Industry data indicates significant shortcomings in the US domestic PV manufacturing capacity. As of the first quarter of 2025, its module production capacity reached 50.5 GW, but its cell production capacity was only 2.3 GW, creating a gap of approximately 37 GW that needs to be filled by imports . Data from the China Photovoltaic Industry Association shows that China accounts for over 75% of global PV module production, and the industry chain cost is about 20% lower than in the US. This supply chain advantage is difficult to replace in the short term.

Facing the potential impact, leading Chinese PV enterprises like Longi and Jinko Solar have already initiated responses, accelerating their global layout in recent years by establishing module factories in regions like the US and the Middle East. Production capacity in new bases such as Saudi Arabia and the UAE is gradually being released.

Fang Wenzheng, an analyst at Longzhong Information, pointed out that US tariff hikes could increase domestic module prices to $0.27-$0.3 per watt, significantly raising costs for power plant operators and consequently hindering its own energy transition process.

Currently, detailed policy rules have not been clarified, and the industry is closely watching the effective date and potential exemption clauses. Relevant personnel from Jinko Solar stated that they have already begun communicating with customers. Auxiliary material companies like Foster are paying attention to the progress of negotiations between Southeast Asian bases and the US.

Market analysis suggests that if the policy is implemented, Chinese PV companies might further shift their focus towards markets in the Middle East and Africa. Simultaneously, US domestic PV project construction could stall due to high costs.

{kind=link}