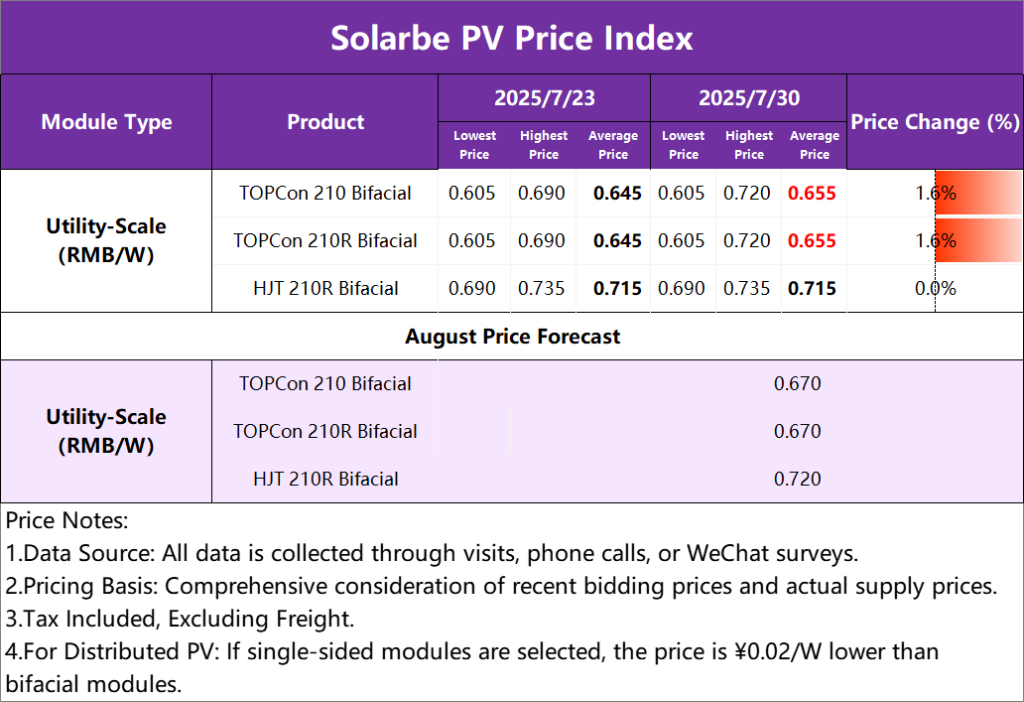

Modules

Module prices rose this week. Utility-scale prices:

- TOPCon 210 Bifacial: ¥0.655/W

- TOPCon Rectangular Bifacial: ¥0.655/W

- HJT Rectangular Bifacial: ¥0.715/W

Supply-Demand Dynamics:

- End-user demand shows no signs of recovery.

- Module manufacturers’ operating rates remain stable, with August output expected to mirror July.

Exports:

- June PV module exports: ~19.22GW (↓6.7% MoM, ↓14.7% YoY).

- Average export price: $0.10/W (flat MoM).

- Jan-Jun total exports: ~119.21GW.

Price Trends:

- Module prices continued rising, driven by upstream polysilicon, wafer, and cell cost increases.

- The Price Law Amendment Draft (July 24) explicitly bans below-cost sales, accelerating industry-wide price hikes.

- Lagged cost transmission from silicon has weakened; cell price surges further pushed up module costs.

- Outlook: Moderate price increases expected next week.

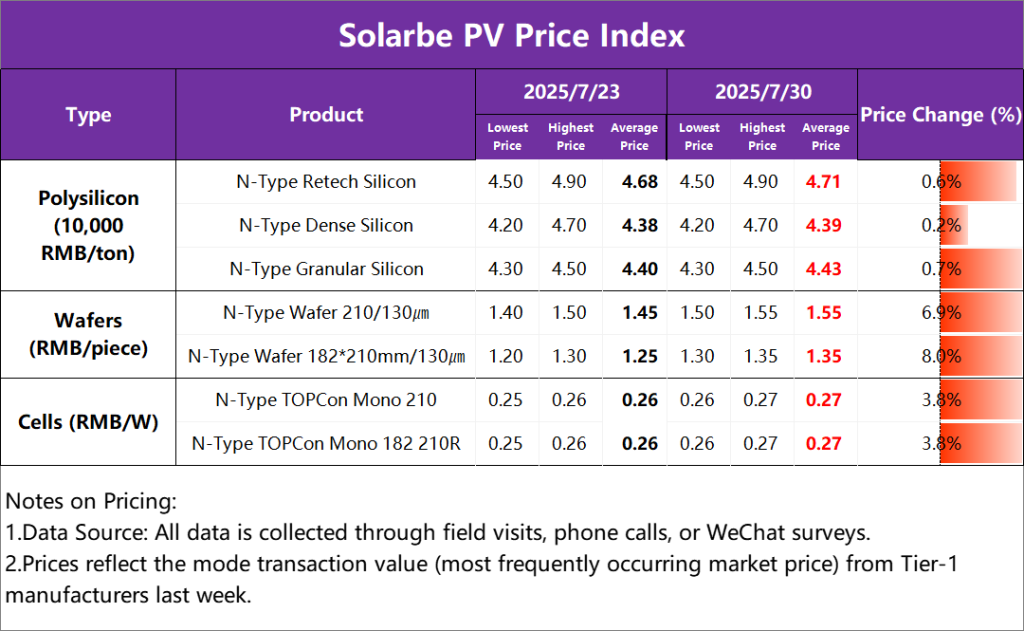

Polysilicon / Wafers / Cells

Polysilicon:

- Prices rose this week:

- N-Type Retech: ¥47,100/ton (avg.)

- N-Type Dense: ¥43,900/ton

- N-Type Granular: ¥44,300/ton

- Supply-Demand: Tier-1 producers maintain output controls, but Tier-2/3 restarts may boost August supply, capping gains. Wafer producers plan output hikes after profit recovery, supporting silicon demand. However, weak module price pass-through and project sensitivity to high costs constrain actual demand.

- Outlook: Moderate price increases next week.

Wafers:

- Prices rose:

- N-Type 210: ¥1.55/pc

- N-Type 182*210mm: ¥1.35/pc

- Supply-Demand: Wafer operating rates hit record lows (Tier-1: 40–50%), with inventories significantly reduced. Cell makers restocked amid “buy-high” sentiment.

- Outlook: Prices to keep rising but at a slower pace due to easing cost pressures and slight supply recovery.

Cells:

- Prices rose:

- N-Type TOPCon 210 Mono: ¥0.27/W

- N-Type TOPCon 210R Mono: ¥0.27/W

- Supply-Demand: Cell inventories dropped to lows; July output ~57GW. Stronger pricing power observed.

- Outlook: Mild increases next week, but narrowing due to slowing cost transmission and nearing terminal acceptance limits.

Notes:

- Data compiled by Solarbe Consulting. Prices are averages. For inquiries, please contact us—discussions welcome.

- Solarbe Consulting updates industry chain price trends every Wednesday/Thursday. Stay tuned!

{kind=link}