Recent years have witnessed simultaneous advancements in solar cell technology shaping the trajectory of encapsulation film development. As a critical auxiliary material for protecting solar cells, photovoltaic (PV) encapsulation films hold significant importance. Module clients now impose stricter requirements on film performance, quality, and stability, while end-users specify supplier rosters in technical tender documents and mandate certifications from internationally recognized third-party testing agencies before bidding.

Though accounting for only 3–7% of module costs, PV encapsulation films substantially enhance photoelectric conversion efficiency and extend component lifespans. Industry data indicate that 1 GW of PV installations require approximately 10–13 million square meters of encapsulation films, projecting global demand to exceed 7 billion square meters by 2025.

After years of development, domestic encapsulation film enterprises have achieved global leadership in technology, scale, and capital. Currently, Chinese firms dominate the global PV encapsulation film supply chain.

“One Superpower, Multiple Strong Players”

The industry has faced dual pressures from raw material price declines and capacity consolidation, leading to a competitive landscape characterized by severe challenges and ongoing integration. The market structure has stabilized, maintaining a “one superpower, multiple strong players” dynamic.

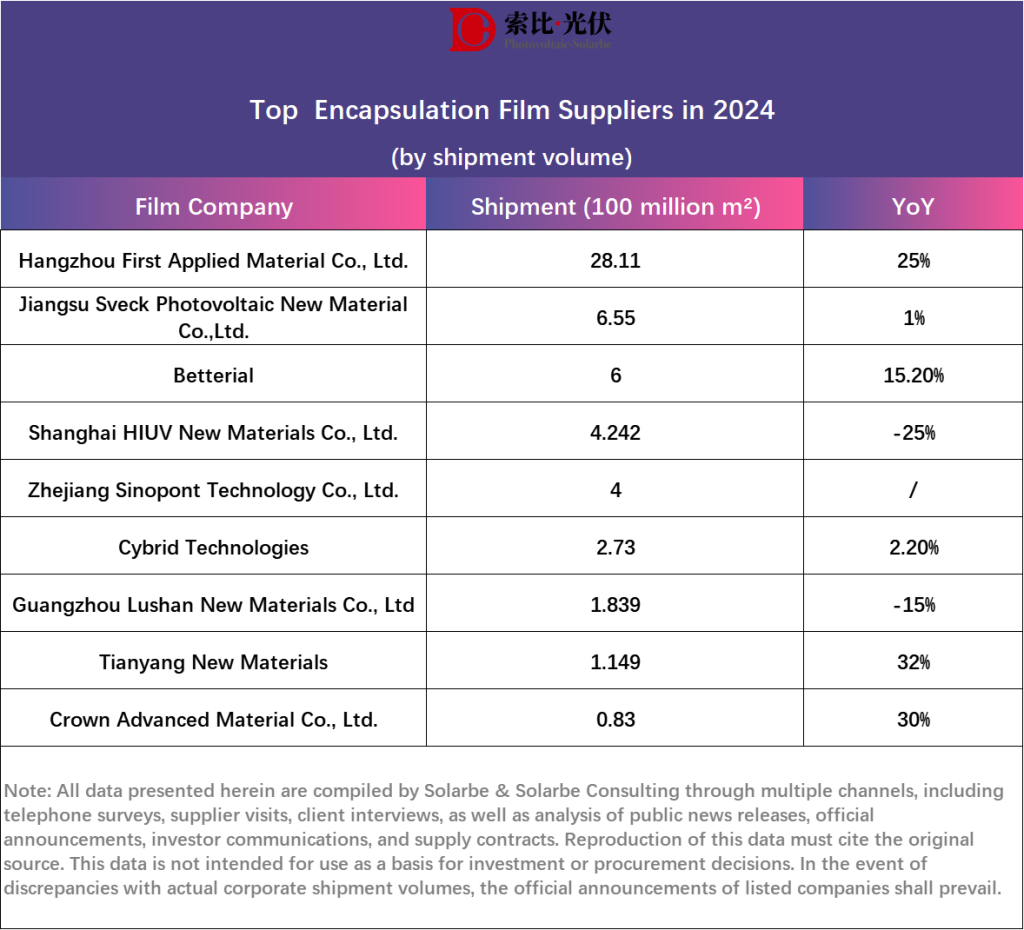

Hangzhou First Applied Material Co., Ltd. (First) leads independently with a dominant market share, technological edge, and capacity scale. In 2024, First shipped 2.881 billion square meters of encapsulation films, a 25% year-on-year increase, translating to 296 GW of encapsulated modules. As the world’s largest PV encapsulation film supplier, First commands around 50% global market share, with cumulative shipments capable of encapsulating over 1,145 GW of PV modules. By 2024, its global capacity exceeded 3 billion square meters, including 600 million square meters of overseas capacity in Vietnam and Thailand.

Jiangsu Sveck Photovoltaic New Material Co.,Ltd. maintained its second-place market share with 655 million square meters sold in 2024, nearly unchanged from the previous year. It operates production bases in Jintan, Suqian, Yancheng (Jiangsu), and Yiwu (Zhejiang), with an annual capacity of 1.276 billion square meters.

Notably, Betterial advanced to third place in encapsulation film shipments, delivering approximately 600 million square meters in 2024, a 15.2% year-on-year increase. It operates six production bases in Changzhou, Yancheng, Chuzhou, Xianyang, Vietnam, and Indonesia, with a planned global encapsulation film capacity exceeding 130 GW.

Shanghai HIUV New Materials Co., Ltd. shipped 424.2 million square meters in 2024, a 25% decline from 2023, attributed to resin price drops, price adjustments for PV encapsulation films, and cautious sales policies to mitigate risks. Cybrid Technologies shipped 273 million square meters, a 2.2% year-on-year increase, with a capacity of 200 million square meters by year-end and a designed capacity of 57 million square meters expected to commence production in September 2025.

Guangzhou Lushan New Materials Co., Ltd shipped 183.9 million square meters, a 15% year-on-year decrease, while maintaining a 400 million square meters/year solar cell encapsulation film capacity. Tianyang New Materials shipped 114.9 million square meters, with annualized capacity reaching 370 million square meters after its Rudong factory commenced operations in June 2024. However, due to declining film prices, it reduced production and halted operations at its Kunshan PV encapsulation film line in 2024.

Crown Advanced Material Co., Ltd. shipped 83 million square meters, a 30% year-on-year increase. By December 2024, it had achieved a 220 million square meters/year encapsulation film capacity, including 100 million square meters/year at its overseas Vietnam base. Its Hefei project, with a 200 million square meters/year capacity, has completed civil engineering, with equipment installation and commissioning pending market conditions.

PV Encapsulation Films Trend Toward Differentiation and Customization

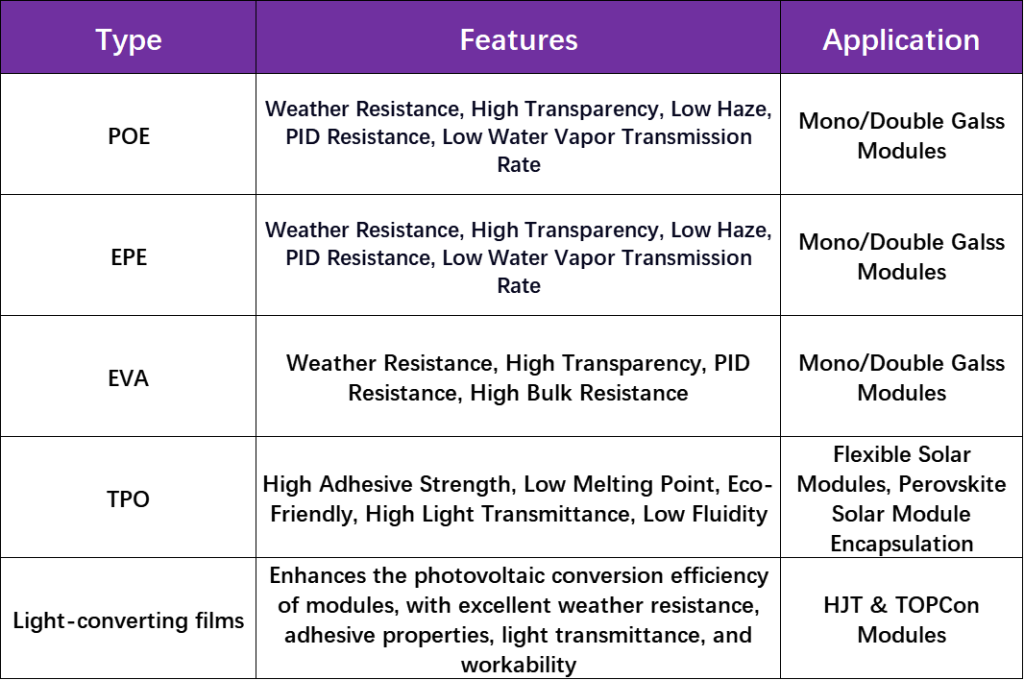

Industry data show that transparent EVA films dominated module encapsulation materials in 2024, with over 40% market share. As TOPCon and dual-glass module market shares rise, co-extruded EPE films’ market share increased to around 37% in 2024, with gradual expansion expected.

Current market film types include transparent EVA, white EVA, POE, and EPE films. In 2024, emerging technologies like BC, HJT, BIPV, and perovskite modules raised technical demands and innovation requirements for encapsulation film enterprises, leading to product diversification and customization. Film characteristics include:

In 2024, TOPCon modules emerged as the mainstream technology in the photovoltaic (PV) industry. However, TOPCon cells are highly sensitive to moisture, prompting the widespread adoption of POE (Polyolefin Elastomer) encapsulants in early applications. The encapsulant configuration for TOPCon modules evolved through three stages: initially, a dual-sided single-layer POE approach was used; this was later replaced by a single-layer POE + single-layer EVA (Ethylene-Vinyl Acetate) hybrid solution; finally, the industry shifted to an EPE (EVA-POE-EVA co-extruded film) + EVA combination to address cost reduction and cross-linking challenges.

Enterprises now focus on developing encapsulation materials for N-type solar cells, covering TOPCon, HJT, perovskite modules, 0BB interconnection technologies, and more. For instance, First launched six new products in 2024, including light-converting films, black films, and innovative co-extruded solutions. For TOPCon, it offers acid-resistant, high-barrier encapsulation solutions. For HJT batteries, it introduced DC-series light-converting films with low UV decay and high power gain.

Sveck’s UV-blocking EVA films, designed for TOPCon batteries, efficiently block UVB light to extend module lifespans and enhance system efficiency. Its latest anti-migration light-converting encapsulation films for heterojunction batteries convert UV light to visible light, boosting module power and stability.

Betterial unveiled desert-specific TOPCon PV module encapsulation films in 2024, addressing UV decay through dynamic hydrogen bonding and customized spectral adaptation. Its Raybo™ light-converting films are becoming standard for HJT modules, with potential applications in heterojunction-perovskite tandem modules.

Lushan New Materials prioritized differentiated innovation in 2024, with light-converting films achieving bulk supply to HJT leaders and black films gaining traction among renowned enterprises. Its BIPV colorful films emerged as a market highlight.

Crown Advanced Material launched heterojunction module high-power light-converting encapsulation films, 0BB battery-specific grid films, and low-acid films for novel TOPCon modules in 2024.

In 2024, falling EVA particle prices drove down PV encapsulation film prices, reducing corporate gross margins. Some firms adjusted production lines to enhance efficiency and quality.

Today, rapid technological iteration, cost-reduction pressures, and operational challenges are accelerating industry consolidation. Firms with outdated technologies and weak competitiveness risk elimination.

During the SNEC exhibition this year, Solarbe Global will engage in in-depth dialogues with leading encapsulation film enterprises, focusing on industry trends, technological innovations, and market developments. The discussions will explore product performance requirements across diverse applications and technical routes. Stay tuned for updates.

{kind=link}