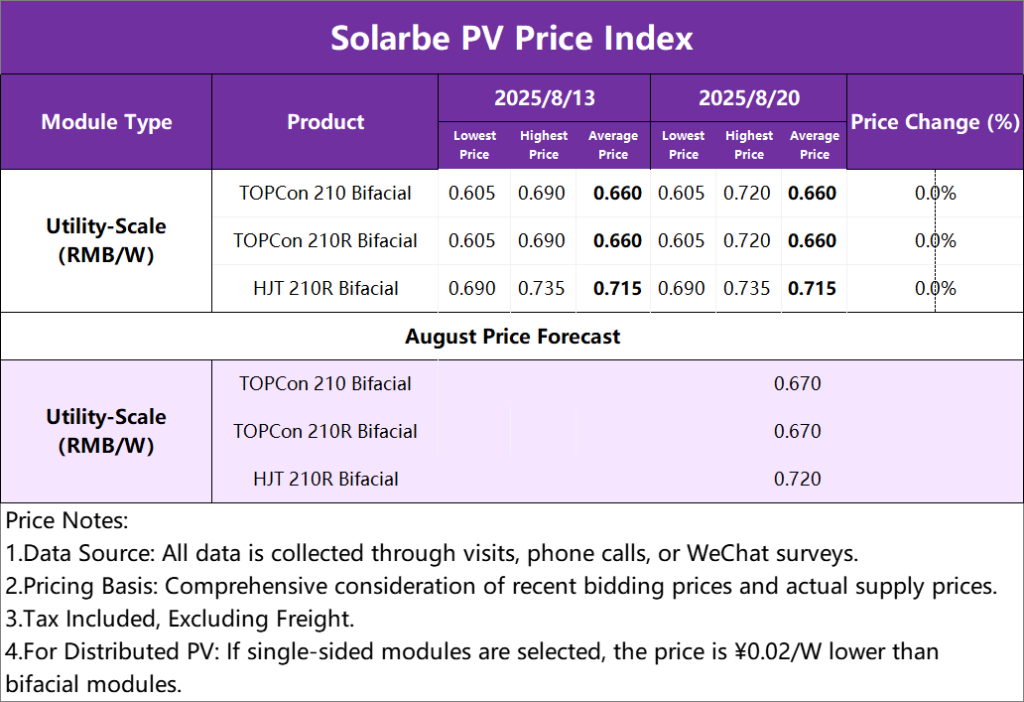

This week, module prices remain unchanged. For ground-mounted power stations, TOPCon 210 bifacial modules are priced at 0.660 yuan/W, TOPCon rectangular bifacial modules at 0.660 yuan/W, and HJT rectangular bifacial modules at 0.715 yuan/W.

On the policy front, on August 19, the Ministry of Industry and Information Technology (MIIT) and five other departments held a symposium on the photovoltaic industry. The meeting emphasized strengthening industrial regulation, curbing low-priced disorderly competition, and focusing on capacity, pricing, and quality, while also enhancing industry self-discipline. This symposium, held 47 days after the photovoltaic manufacturing enterprise symposium on July 3, saw the participation of additional departments, highlighting a deepened focus on “anti-involution” policies in the photovoltaic industry. The clearance of photovoltaic capacity and technological iteration will become the main themes of structural market trends.

Regarding tenders, on August 18, China Resources Power opened bids for its second centralized procurement of photovoltaic module equipment in 2025, with a procurement scale of 3GW. The average bid price for Lot 1 was 0.729 yuan/W, for Lot 2 it was 0.729 yuan/W, and for Lot 3 it was 0.718 yuan/W. The average bid price this time showed an increase compared to previous tenders, indicating that price pass-through to the end user is expected to materialize.

In terms of pricing, first-tier module manufacturers have quoted prices as high as 0.7 yuan/W. Although quoted prices have risen, the actual mainstream transaction prices mostly remain in the range of 0.65–0.68 yuan/W. The average bid price for China Resources Power’s 3GW module procurement was significantly higher than the market price at the time, sending a positive signal to the market and boosting module manufacturers’ confidence in raising prices. It is expected that photovoltaic module prices will continue to maintain a stable and slightly upward trend in the short term.

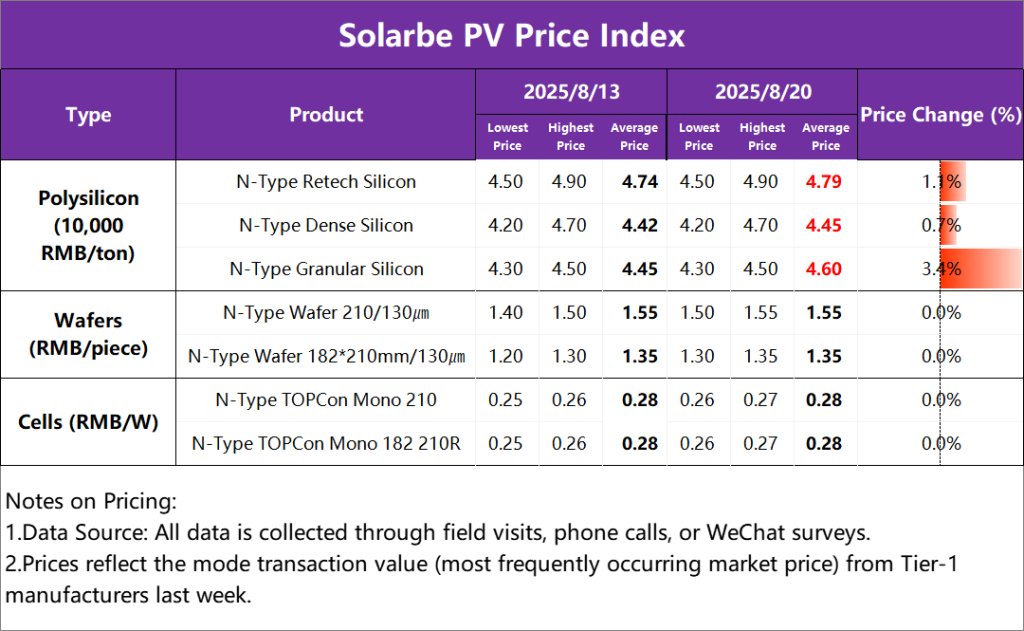

This week, silicon material prices rose. The average price of N-type recycled materials is 47,900 yuan/ton, N-type dense materials average 44,500 yuan/ton, and N-type granular silicon averages 46,000 yuan/ton.

In terms of supply and demand, data from the Silicon Industry Branch shows that silicon material production may increase to 140,000 tons in September, exacerbating the supply-demand imbalance. Silicon material inventory has risen for two consecutive weeks, increasing the pressure of accumulation on an already high base. Under inventory pressure, silicon material prices are expected to remain under pressure with weak stability in the short term.

This week, silicon wafer prices remain unchanged. The average price of N-type 210 silicon wafers is 1.55 yuan/piece, and N-type 182*210mm silicon wafers average 1.35 yuan/piece.

In terms of supply and demand, although inventory in the silicon wafer segment is relatively healthy for now, weakening demand in the future may bring risks of inventory accumulation. High and stable silicon material prices provide cost support for silicon wafer prices. Purchase orders for silicon wafers are limited, and market transactions are weak. It is expected that silicon wafers will face overall pressure in the short term, maintaining a weak and stable pattern, with prices for certain sizes, especially large-size silicon wafers, at risk of slight adjustments.

This week, solar cell prices remain unchanged. The average price of N-type TOPCon monocrystalline 210 cells is 0.28 yuan/W, and N-type TOPCon monocrystalline 210R cells average 0.28 yuan/W.

In terms of supply and demand, the solar cell market is currently under pressure due to divergent cost support, unsuccessful attempts by downstream modules to raise prices, and weak end-user demand. Prices are generally reported as stable but are under palpable pressure. Demand for large-size cells is relatively weak and has not provided strong support for the 210 series cells. In the short term, cell prices are expected to face overall pressure, with prices for large-size cells such as 210 facing significant downward risks due to upstream loosening and weak demand.

{kind=link}