Core Data Insights

The photovoltaic module industry is currently in a period of deep adjustment. Overall, the Matthew effect of “the strong getting stronger” is intensifying, while the entire industry faces significant pressure from overcapacity.

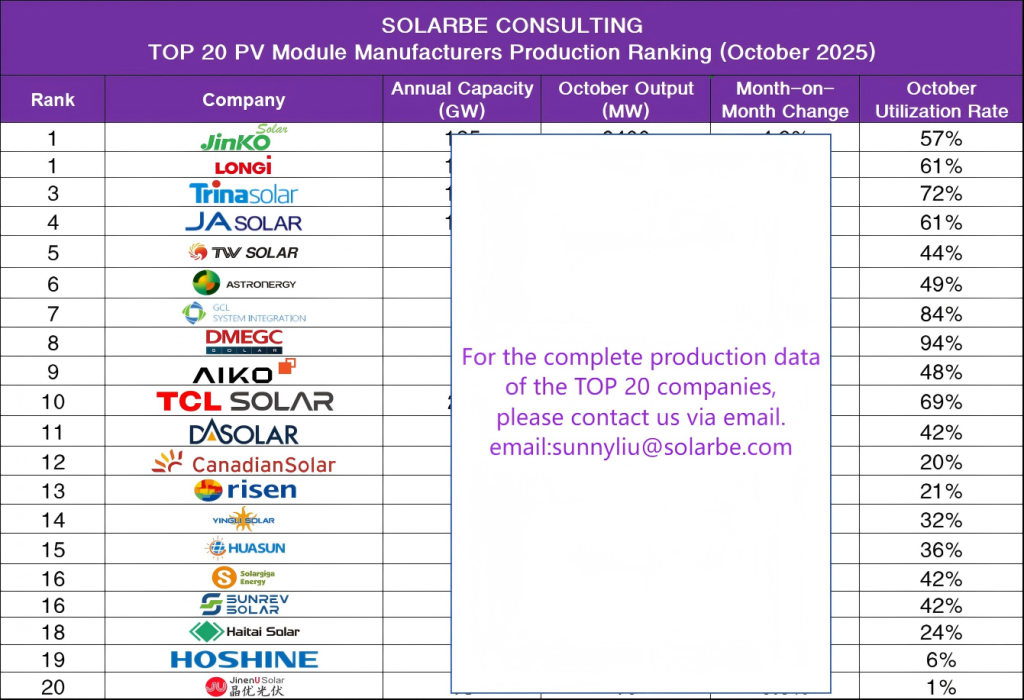

- Industry-Wide Pressure, Persistently Low Operational Rates: In October, as many as 13 of the TOP 20 companies had operational rates below 50%, with the industry average around just 45%. This indicates that over half of the industry’s capacity is idle, with structural overcapacity being the core contradiction.

- Solidified Top Tier, Formation of a ‘One Dominant Leader, Several Major Players’ Landscape: Trina Solar, Jinko, LONGi, and JA Solar form a stable first tier, with monthly outputs far exceeding others. Among these leaders, Trina Solar’s operational rate remains the highest. Notably, Jinko and LONGi achieved month-on-month output growth in October, a notable feat in the weak market.

- Severe Divergence Among Companies, Tough Survival for the Tail-End:

- Tail-End Company Crisis: Canadian Solar, Aiko Solar, and Chint Group experienced double-digit month-on-month declines. Companies like Jingyou and Hoshine Silicon have seen their operational rates fall to single digits, with very low monthly output. In a PV industry where economies of scale are crucial, such companies face the most severe survival tests.

Q4 2025 Trend Forecast

- Accelerated Capacity Rationalization and Industry Consolidation: Driven by persistent losses and policy guidance, destocking and capacity reduction remain the main themes. With monthly output from tail-end companies already below 500MW, it is foreseeable that within the next 1-2 years, some less competitive enterprises will be forced out or consolidated. Market share will further concentrate towards leading companies and those with core advantages.

- Technological Competition Becomes Key to Breaking the Deadlock: While “price wars” will continue, the competitive focus will shift from price alone to comprehensive strength in “technology, brand, and reliability.” The replacement of P-type by N-type technology will be largely complete. The mass production efficiency and cost advantages of advanced technologies like BC cells, TOPCon 2.0, HJT, and perovskite will become the core weapons for leading companies to widen the gap and improve profitability.

- Limited Optimism for Prices and Profits: Upstream prices are expected to stabilize with continued “anti-internal volume” policies and deepened industry self-discipline. However, as end-demand is highly price-sensitive, rising upstream costs will be difficult to fully pass through to the module end. Profit margins for module manufacturers will remain under pressure.

- Emphasis on Both Policy and Globalized Layouts: Domestically, the formal submission of China’s NDC 3.0 is expected to drive improved medium-to-long-term installation demand. Simultaneously, companies will pay more attention to balancing overseas expansion with the domestic market. Companies with strong overseas production layouts and channels (e.g., Jinko, Trina, Canadian Solar) will demonstrate greater resilience.

{kind=link}