Price is crucial to photovoltaic industry.

In 2020, with the advent of parity, the price has been the talk of the photovoltaic industry. Affected by the pandemic at the beginning of the year, the demand of domestic and foreign photovoltaic market was depressed as a whole. There was also an explosion happened in silicon factory in the middle of the year.

In addition, due to a series of uncontrollable factors such as natural disasters and pandemic, silicon prices soared. In July, photovoltaic glass then became the focus of price increase. This year, photovoltaic products experienced price fluctuations like riding on roller coaster.

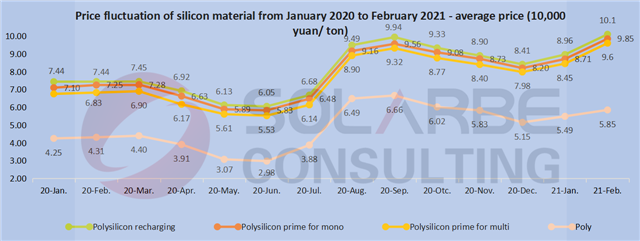

Silicon material

The price of silicon material began to show a downward trend in March 2020, and reached the lowest point in June. Some production capacity has stopped, and overseas production gradually withdrew.

Since July 2020, the leading enterprises have been carrying out production line maintenance in succession, and the production was hindered. In addition, the new production capacity was limited, and the supply of silicon materials was in short supply. The price began to soar, and reached peak in late August. The price of recharging material has exceeded 100,000 yuan/ton, increased by 11% compared with the beginning of the year.

Since August 2020, the production line has been overhauled in succession, the production capacity has been restored, and the price of silicon material has slowly come down. The price of polysilicon prime for mono material at the end of the year reached 82,000 yuan/ton, which was still about 10,000 yuan higher than that at the beginning of the year.

In 2021, the enterprises began to prepare goods before the Spring Festival, increased raw material inventory, carried out pandemic control in various places during the holiday, and stopped some logistics, which led another silicon material price rise that has continued at the end of February.

The average price of polysilicon prime for mono material increased from 82,000 yuan/ton at the end of 2020 to 98,500 yuan/ton in February 2021, with the highest quotation of 107,000 yuan/ton; The average price of disposable material increased from 51,500 tons at the end of 2020 to 58,500 yuan/ton at the end of this February, with the highest price of 59,000 yuan/ton.

In 2021, the prosperity of silicon materials will remain high, as well as the price, and the supply and demand will be in a tight balance.

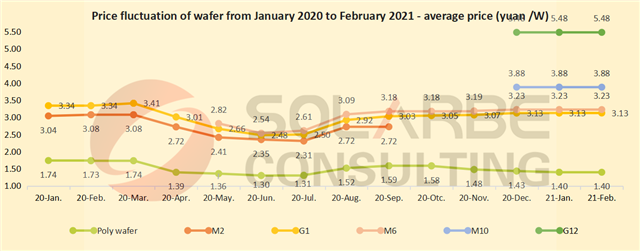

Wafer

In the first half of 2020, due to the impact of the overseas pandemic, the demand for modules was weak and transmitted to the upstream, and the price of silicon wafers fell. Taking Longi as an example, its quotation has been lowered many times.

In June, the lowest quotation for G1 monocrystalline silicon wafer was 2.53 yuan/piece, and the average market transaction price was as low as 2.48 yuan/piece. Since the middle of the year, due to the installation rush, together with the rising price of silicon materials, the price of silicon wafers has continued to rise. The price of mainstream G1 and M6 wafers is about 0.8 yuan higher than that at the beginning of the year.

In 2020, monocrystalline silicon wafer enterprises expanded their production rapidly, with huge new production capacity, especially the large-size modules of M10 and G12. The iteration of new and old production capacity forced G1 to reflect its price advantage. From the beginning of mass production, its price was close to M2. In June, the price difference between the two is only 0.13 yuan. By September, M2 was completely replaced.

By the end of 2020, a large number of downstream wafers were expanded, and the demand for silicon wafers was strong. In addition, the supply of upstream silicon materials was tight, and the price of silicon wafers remained high until 2021.

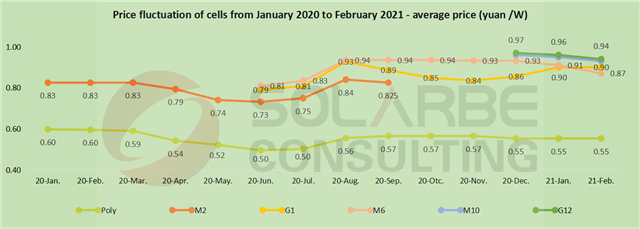

Cell

The supply and demand situation of cells is similar to that of silicon materials. It was quite expensive at the beginning of 2020. Affected by supply and demand, the price of cell in the first half of the year decreased by about 0.1 yuan, and reached the bottom in the middle of the year. Since July, the prices of silicon materials and wafers have increased, and the price of cells recovered to the level at the beginning of the year, and reached the peak in August. However, the price of polycrystalline cells continued to decline due to the impact of capacity iteration.

At the same time, HJT, Topcon and other new technologies are gradually emerging, and become a new generation of battery technology when PERC approaching its limit.

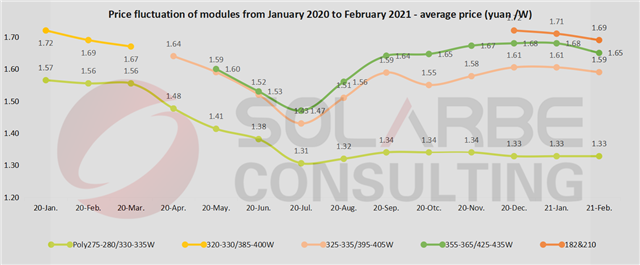

Module

At the beginning of 2020, the operating rate of the module end was low, the overseas pandemic situation was serious, and the internal logistics was blocked, as well as the export. In the first half of the year, the price remained low.

At the beginning of 2021, the price of auxiliary materials remained at a high level, and the price of upstream cells declined with a limit. The module price in January was basically the same as that at the end of the 2020. It is expected that this year’s module will produce excess capacity, and prices will decline.

Glass

Glass, the most popular auxiliary material of photovoltaic industry in 2020. Due to the demand for glass for bifacial modules and large-size modules, price increases became a common occurrence in the second half of the year.

The appearance of large-size modules puts forward new requirements for the size of glass. In the past decade, the requirements of photovoltaic modules for glass size were relatively stable, and basically four sizes could cover all the requirements. In order to reduce cost and improve efficiency, the length of production line was limited, which limited the space of size increase.

{kind=link}