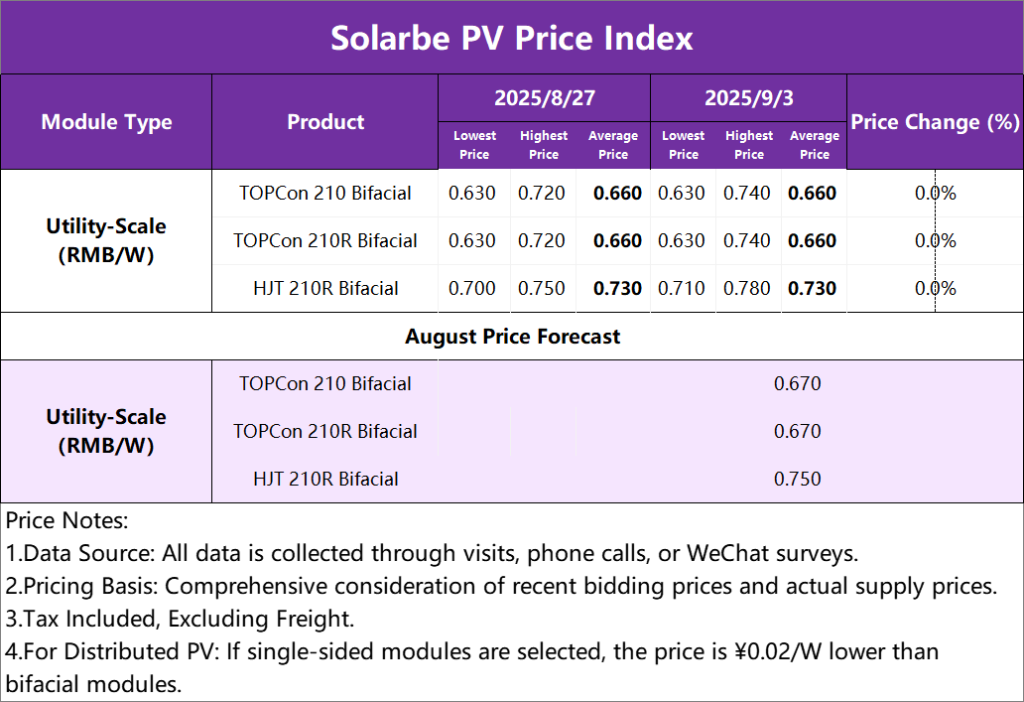

Modules

In terms of supply and demand, end-user demand remains insufficient. In July, China’s newly installed photovoltaic capacity decreased by 23.12% month-on-month and 47.55% year-on-year. Recently, there has been little change in the operating rates of module manufacturers. September module production schedules show no significant increase compared to August and are largely flat. Demand during the traditional peak season is expected to be lower than in previous years. Many power groups have already met their targets under the “14th Five-Year Plan,” leading to subdued demand expectations. Inventory pressure on modules has increased, with second- and third-tier manufacturers facing significant challenges in shipments.

Exports

In July, photovoltaic module exports reached approximately 20.12 GW, up 4.7% month-on-month but down 1.1% year-on-year. The average export price of modules was $0.09/W, declining month-on-month. From January to July, total module exports reached about 141.51 GW.

Prices

From late August to early September, the photovoltaic module market exhibited a trend of upstream cost-driven price increases, coupled with limited acceptance from downstream demand. Although prices across the industrial chain rose after a joint meeting of six government departments on the photovoltaic industry, the actual transaction volume remained low due to relatively singular end-user demand and limited acceptance of higher prices. In the short term, module prices are expected to enter a phase of stabilization, with limited room for both increases and declines.

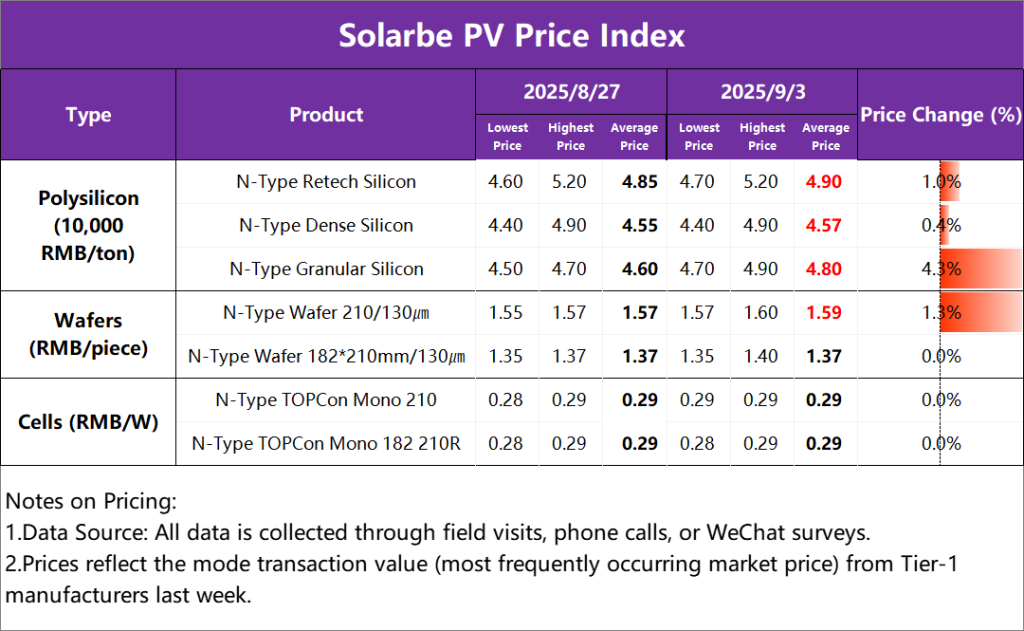

Silicon Material / Silicon Wafers / Cells

This week, silicon material prices increased. The average price of N-type recycled materials was RMB 49,000/ton, N-type dense materials averaged RMB 45,700/ton, and N-type granular silicon was RMB 48,000/ton.

In terms of supply and demand, recent production cuts have been intensified. Data from the Silicon Industry Branch shows that silicon material output in September is expected to be around 125,000–130,000 tons, a decrease of about 7%–10% from the original plan. Although silicon material transactions saw an increase in late August, they temporarily declined in September as self-regulation measures took effect, with procurement mainly focused on small-scale stockpiling. Inventory pressure persists, with 350,000–400,000 tons of inventory across the industry yet to be digested. Production capacity remains significantly higher than downstream demand. The tug-of-war between silicon material producers’ intention to maintain prices and downstream acceptance will intensify.

This week, silicon wafer prices rose. The average price of N-type 210 silicon wafers was RMB 1.59/piece, while N-type 182*210mm silicon wafers averaged RMB 1.37/piece.

In terms of supply and demand, domestic silicon wafer production increased in August, with integrated enterprises significantly ramping up production and specialized silicon wafer manufacturers slightly increasing output. Based on research, silicon wafer production schedules for September are expected to show a slight increase. Silicon wafer inventory has shifted from destocking to slight accumulation, though overall inventory remains at a reasonable level. Upstream polysilicon prices continue to hold firm due to industry self-regulation agreements, and despite sustained declines in the price of raw material industrial silicon, costs for silicon wafers remain supported. Against the backdrop of firm polysilicon prices, leading silicon wafer companies are considering a second round of price hikes. Although silicon wafer prices are attempting to hold firm, downstream cell and module segments have limited acceptance of higher prices. In the short term, silicon wafer prices are expected to remain stable overall, with the possibility of slight试探性 increases, though differentiation between models will continue.

This week, cell prices remained unchanged. The average price of N-type TOPCon monocrystalline 210 cells was RMB 0.29/W, while N-type TOPCon monocrystalline 210R cells also averaged RMB 0.29/W.

In terms of supply and demand, cell production schedules for September are approximately 59 GW, up about 2% month-on-month from August. With rising prices, manufacturers have little intention to reduce production, and integrated plants have increased output significantly. In the short term, cell market prices are expected to remain stable overall, though performance will vary significantly by model. Demand for 210 cells is relatively strong, with prices holding firmer, while 210RN cells face pressure due to high inventory and weak demand, making price increases difficult and likely to remain under pressure.

Note:

- Data compiled by SOLARBE Consulting. Prices are averages. Please contact us with any questions or for discussion.

- SOLARBE Consulting updates industrial chain price trends every Wednesday and Thursday. Stay tuned.

{kind=link}