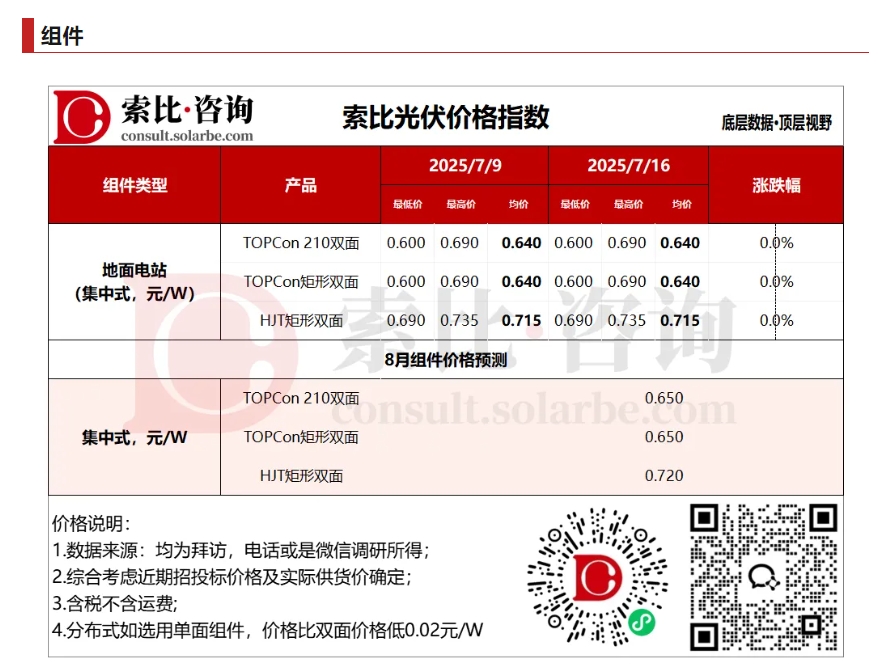

This week, module prices remained unchanged. For utility-scale projects, TOPCon 210 bifacial modules averaged RMB 0.640/W, TOPCon rectangular bifacial modules averaged RMB 0.640/W, and HJT rectangular bifacial modules averaged RMB 0.715/W.

Demand: The domestic distributed market remained sluggish, while centralized projects relied on existing orders. Overseas markets were cautious, with limited improvement expected in September. Overall, supply-demand dynamics showed slight recovery but remained oversupplied.

Supply: Module production in July is projected to dip slightly compared to June. In August, both domestic and international markets are expected to remain in a seasonal demand lull, with operating rates likely to decline modestly.

Prices: Upstream silicon material quotations surged sharply, and wafer manufacturers raised prices in tandem, driving up module costs. However, end-market acceptance was limited. Due to cost pressures and policy drivers, module prices may attempt a moderate rise next week, but weak demand and high inventory levels will likely cap the increase.

Silicon Material Prices Rose This Week:

- N-type recycled material averaged RMB 42,000/ton,

- N-type dense material averaged RMB 39,000/ton,

- N-type granular silicon averaged RMB 40,600/ton.

Price Trends: Driven by “anti-internal competition” policies, silicon material producers collectively raised prices. Leading firms with cost advantages pushed for hikes, while high-cost producers struggled to secure deals. On the supply-demand front, environmental restrictions in Xinjiang and slower-than-expected resumption in Southwest China reduced monthly silicon output to 100,000 tons, though inventories remained high. Downstream wafer producers only replenished stocks modestly, while module prices stabilized, and end-market acceptance of price hikes was low. Under policy pressure, silicon material prices are expected to maintain a “steady quotation, slow transaction increase” trend in the short term.

Wafer Prices Rose This Week:

- N-type 210 wafers averaged RMB 1.35/piece,

- N-type 182*210mm wafers averaged RMB 1.15/piece.

Price Trends: Wafer prices saw a substantial increase, driven by upstream silicon material hikes and “anti-internal competition” policy expectations. While trading activity improved, resistance from downstream cell producers intensified. Considering policy continuity, cost support, and supply-demand dynamics, wafer prices are expected to continue rising in the short term but at a slower pace, entering a moderate upward trajectory.

Cell Prices Rose This Week:

- N-type TOPCon monocrystalline 210 cells averaged RMB 0.25/W,

- N-type TOPCon monocrystalline 210R cells averaged RMB 0.25/W.

Price Trends: Cell prices ended their long-term decline this week, rebounding on policy-driven momentum. Central government directives accelerated capacity phase-outs, with silicon material, wafer, and cell sectors jointly supporting price hikes. Cell manufacturers slowed shipments to mitigate losses, while wafer price increases exceeding 10% directly raised production costs. Despite low inventories, cell producers ramped up wafer procurement amid full-capacity operations, though module-end acceptance remained weak, intensifying negotiations. In the short term, cell prices are expected to continue rising but with narrower gains, as module-end acceptance nears its limit.

Notes:

- Data compiled by Solarbe Consulting. Prices are averages. For inquiries or discussions, please contact us.

- Solarbe Consulting updates industry chain price trends every Wednesday and Thursday. Stay tuned.

{kind=link}