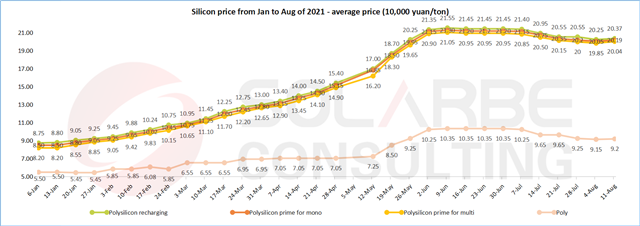

Silicon

After five consecutive weeks of price reduction, the operating rate of silicon wafer enterprises increased due to the rise of demand, and the silicon material price rebounded slightly this week.

According to the statistics of Solarbe Consulting, the domestic silicon material output was 42,000 tons in July, and some enterprises planned maintenance in August. The output is expected to decrease slightly, without serious impact. The output in August was about 41,000 tons. In 2021, the total output of silicon material in China is about 500,000 tons, and the remaining total output this year is about 200,000 tons. Compared with the installation demand, there is a gap of 100,000 tons that needs to be supplemented by foreign imports.

This week, the average price of monocrystalline recharging material was RMB 203,700 yuan/ton, up 0.60% month on month, 201,900 yuan/ton for polysilicon prime for mono, up 0.72% month on month, and 200,400 yuan/ton for polysilicon prime for multi, up 0.94% month on month. The average price of polycrystalline materials was 92,000 yuan/ton, up 0.55% month on month.

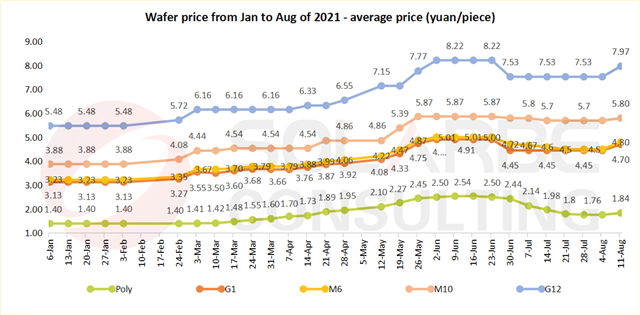

Wafer

This week, silicon wafer prices rose in an all-round way. Due to the limited supply of silicon material, even if enterprise has a certain amount of silicon wafer inventory, the overall supply of wafer is limited by silicon. When the downstream demand is pulled up, the seller’s market tends to be obvious.

The average price of G12 was RMB 7.9 yuan/piece, up 5.84% month on month, 5.80 yuan/piece for M10, up 1.75% month on month, 4.80 yuan/piece for M6, up 6.67% month on month, and 4.70 yuan/piece for G1, up 5.62% month on month. The average price of polysilicon wafer was RMB 1.84 yuan/piece, up 4.26% month on month.

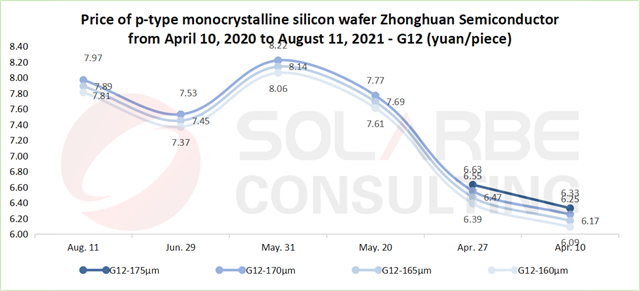

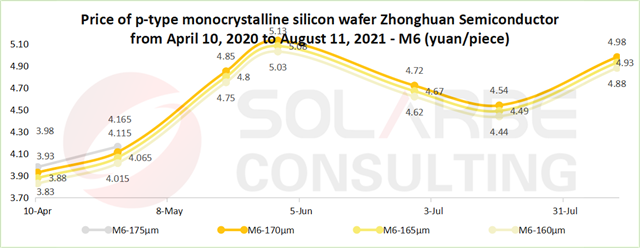

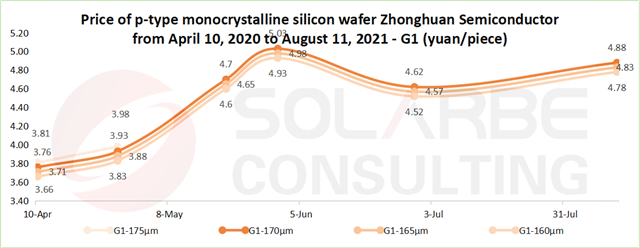

On August 11, Zhonghuan Semiconductor announced the latest price of silicon wafers. Compared with the quotation on June 29, the price of all thickness of G12 increased by RMB 0.44 yuan/piece, and that of all thickness of G1 increased by RMB 0.26 yuan/piece; Compared with the quotation on August 11, all thickness of M6 was increased by RMB 0.44 yuan/piece, an increase of nearly 10%.

The price of G12 of 170μm was RMB 7.97 yuan/piece, up 5.84% month on month;

The price of G12 of 165μm was quoted at RMB 7.89 yuan/piece, up 5.91% month on month;

The price of G12 of 160μm was RMB 7.81 yuan/piece, up 5.97% month on month.

The price of M6 of 170μm was RMB 4.98 yuan/piece, up 9.69% month on month;

The price of M6 of 165μm was RMB 4.93 yuan/piece, up 9.80% month on month;

The price of M6 of 160μm was RMB 4.88 yuan/piece, up 9.91% month on month.

On July 17, Zhonghuan only released the price of M6. Compared with the price released on June 29, the wafer of all thickness was reduced by RMB 0.18 yuan/piece. But this time, on the basis of returning to the original price, it has been increased by RMB 0.26 yuan/piece. Based on the clear judgment that large-sized M10 and G12 are the mainstream of the future market, the price of M6 has fallen rapidly in the past month and a half. The owner is on the sidelines, and the manufacturers are desperate to sell, resulting in the structural shortage of M6. However, according to Solarbe Consulting, the price of M6 of Longi has not been raised. The purpose is to accelerate the elimination of M6 and complete the upgrading and transformation of all production capacity.

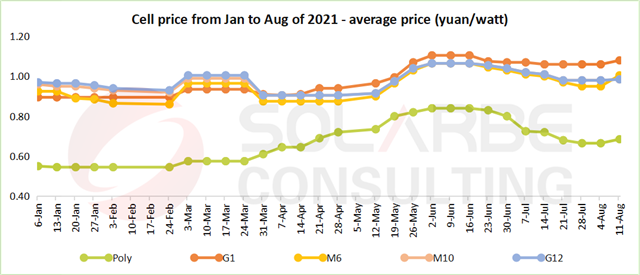

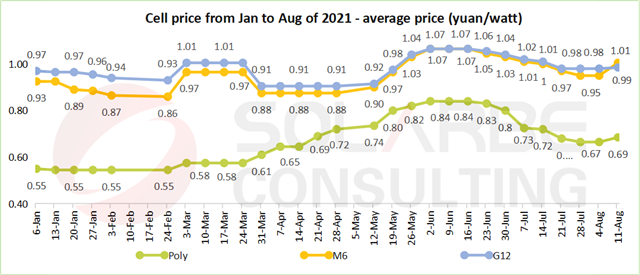

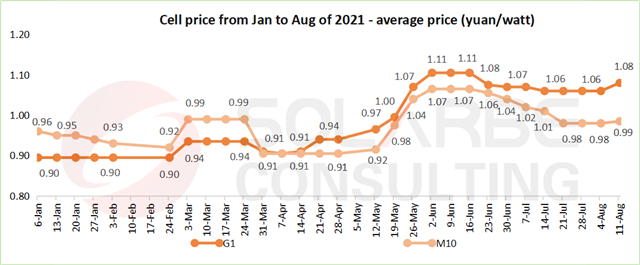

Cell

This week, the price of cells rose, and M6 rose the most. Since the markup of silicon materials, cell manufacturers gradually starts to take pressure. The upstream silicon wafers directly transferred the cost, and the downstream modules may refuse to set more orders if the prices are not satisfactory, resulting in cell enterprises suffering serious losses, especially manufacturers only producing cells.

This week, the average price of G12 and M10 was RMB 0.99 yuan/W, up 0.51% month on month, 1.08 yuan/W for G1, up 3.01% month on month, and 1.01 yuan/W for M6, up 5.79% month on month. The average price of polycrystalline cells was RMB 0.69 yuan/W, up 3.01% month on month.

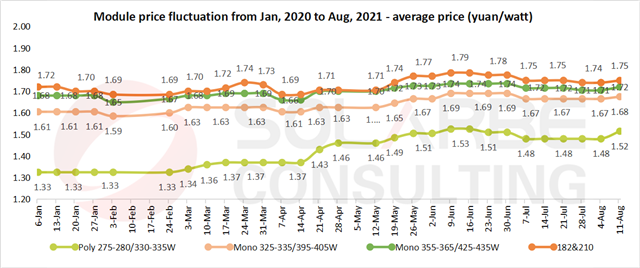

Module

With the increasing demand, the operating rate of the module end is the first to recover. Due to the pull of terminal demand, the prices of silicon, wafer and cell have been increased. Even if the price of silicon material is stable below 210,000 yuan/ton, the increase of wafer price has brought great pressure to the cell and module link. Although the module price increases, it is difficult for the terminal to accept higher module prices.

From the installed capacity in the first half of this year, even though with large bidding scale, the number of actual settled projects is small. According to the data released by the National Energy Administration, in the first half of this year, the installed capacity reached 13 GW, mainly are distributed projects, and the newly installed capacity of large scale power stations was even lower than that in the same period last year. On the one hand, it shows that the price rise has affected the installed capacity; on the other hand, there is an installed capacity of more than 40 GW in the second half of the year. Such a scale needs to be supported by stable and reasonable prices.

The average price of 182-210mm monocrystalline modules this week was RMB 1.75 yuan/W, up 0.57% month on month; 1.72 yuan/W for 355-365/425-435W, up 0.88% month on month; 1.68 yuan/W for 325-335/395-405W, up 0.60% month on month. The average price of polycrystalline 275-280/330-335W modules was RMB 1.52 yuan/W, up 2.36% month on month.

About Solarbe Consulting

Relying on Solarbe, the authoritative media in the photovoltaic industry, Solarbe Consulting focuses on data and industry research. It provides photovoltaic enterprises with market data, enterprise consulting, price trend, enterprise analysis, market research, customized report and other services, helping enterprises make correct decisions in sales, production, expansion and decision-making.

{kind=link}