The International Energy Agency’s Photovoltaic Power Systems Programme (IEA PVPS) recently released its “Global PV Market Outlook 2025” report, revealing that the global photovoltaic (PV) market demonstrated robust growth in 2024, with installed capacity surging and market demand continuing to expand, injecting strong momentum into the global energy transition.

By the end of 2024, global cumulative installed PV capacity rose from 1.6 terawatts (TW) in 2023 to over 2.2 TW, with new PV system installations exceeding 600 gigawatts (GW). This data underscores the growing importance of the PV industry within the global energy mix. After years of tight raw material and transportation costs, module prices continued to decline amid a market imbalance between supply and demand. While this situation has placed significant financial pressure on enterprises across the entire industry chain, it has also stimulated market demand, enabling more countries and regions to deploy PV systems at lower costs.

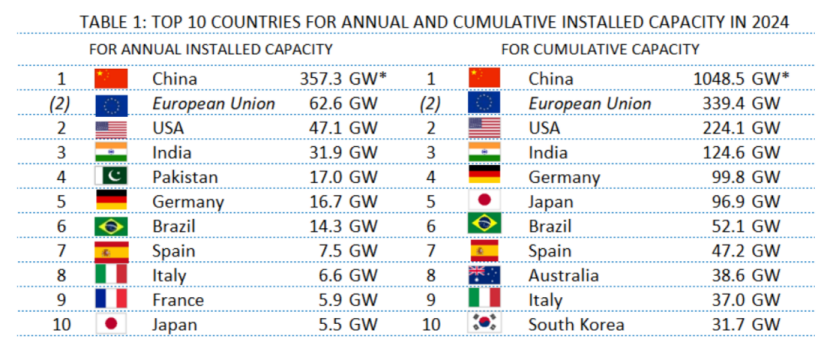

Regionally, at least 34 countries worldwide installed over 1 GW of new PV capacity in 2024, up from 29 in 2023. Currently, 25 countries have exceeded a cumulative installed capacity of 10 GW, with seven surpassing 40 GW.

Driven by policy support, China’s annual new installed capacity climbed to 357.3 GW in 2024 (higher than the 277.57 GW previously announced by the National Energy Administration), accounting for approximately 60% of global new installations. By the end of 2024, China’s PV installed capacity represented nearly half of the global total, cementing its role as the core driver of global PV market development.

The European market maintained strong growth, led by Germany (16.7 GW) and Spain (7.5 GW). In the Americas, both the United States and Brazil achieved notable growth, with the U.S. installing 47.1 GW of new PV capacity in 2024, ranking third, while Brazil added 14.3 GW to reach a cumulative installed capacity of 52.1 GW.

In the Asia-Pacific region, India installed 31.9 GW of new capacity in 2024, primarily concentrated in utility-scale projects. Pakistan reached 17 GW of installed capacity within four years. However, growth in other Asia-Pacific markets, such as Australia (4 GW) and Japan (5.5 GW), slowed.

As PV installed capacity growth outpaced electricity consumption growth, the theoretical power generation penetration rate of PV continued to rise globally. Currently, PV installed capacity in over 25 countries meets more than 10% of domestic electricity demand, with nearly half of these countries approaching or exceeding a 20% penetration rate.

In countries with high PV penetration rates, curtailment of PV-generated electricity is becoming increasingly common. To fully utilize peak generation capacity, future efforts will focus on grid expansion and upgrades, cross-regional interconnection, flexibility improvements, energy storage technologies, and multi-sector coupling. Given that curtailment is driven by both technical factors (power supply imbalances) and market factors (negative pricing), power generators offering diversified services (hybrid systems, capacity reserves, system services) are likely to become a critical pathway for maintaining long-term profitability.

Looking ahead to 2025, PV installations are expected to continue growing steadily or moderately in most IEA PVPS member countries. However, policy adjustments may impact certain markets. France, Switzerland, Sweden, Austria, and the United States, through policy changes such as reduced feed-in tariffs and investor support mechanisms, could face adverse effects, though market forces and further development of power purchase agreements (PPAs) should mitigate potential volatility. In contrast, policy adjustments in other countries, such as Japan and Australia, may support stronger growth.

{kind=link}