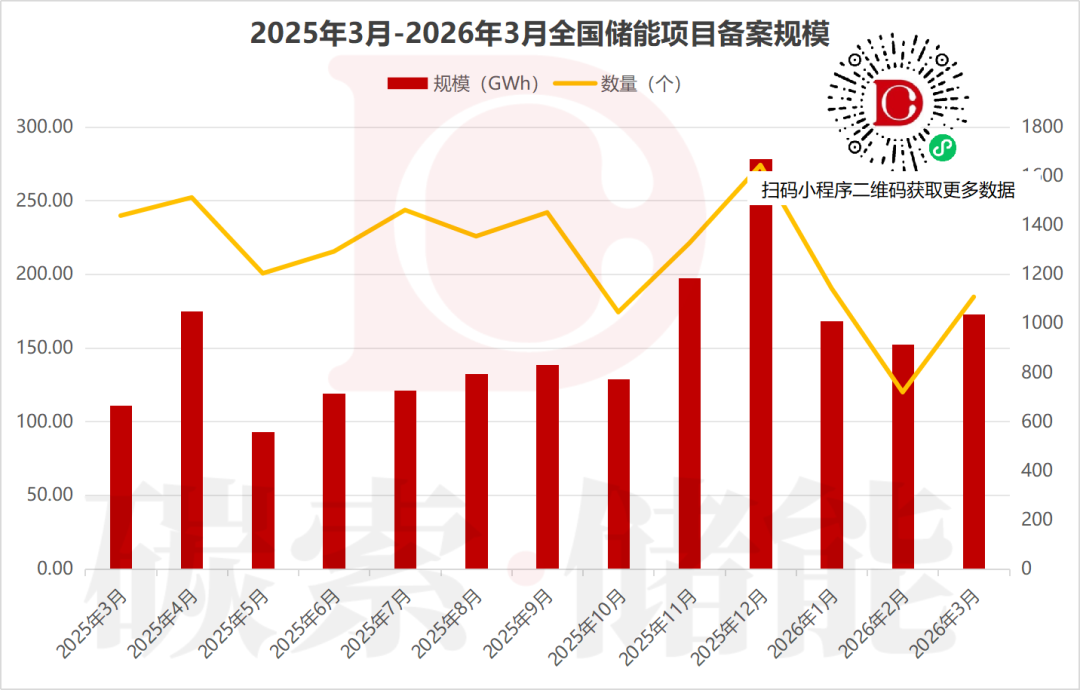

The first quarter of 2026 ends, and the energy storage market remains hot. In March, according to incomplete statistics of the carbon cable energy storage network, the domestic energy storage project filing scale reached 172.75GWh, a total of 1107 projects, the market rebounded quickly after a short correction during the Spring Festival holiday, demonstrating strong resilience.

1. overall scale: rapid rebound, demonstrating market resilience

In the past year, the scale of energy storage filing has shown periodic fluctuations. After hitting a peak of 278.12GWh in December 2025, the scale fell continuously in January and February 2026 due to the influence of the Spring Festival. March data quickly rebounded to 172.75GWh, confirming that market demand fundamentals are solid and corporate investment enthusiasm quickly recovered after the holidays.

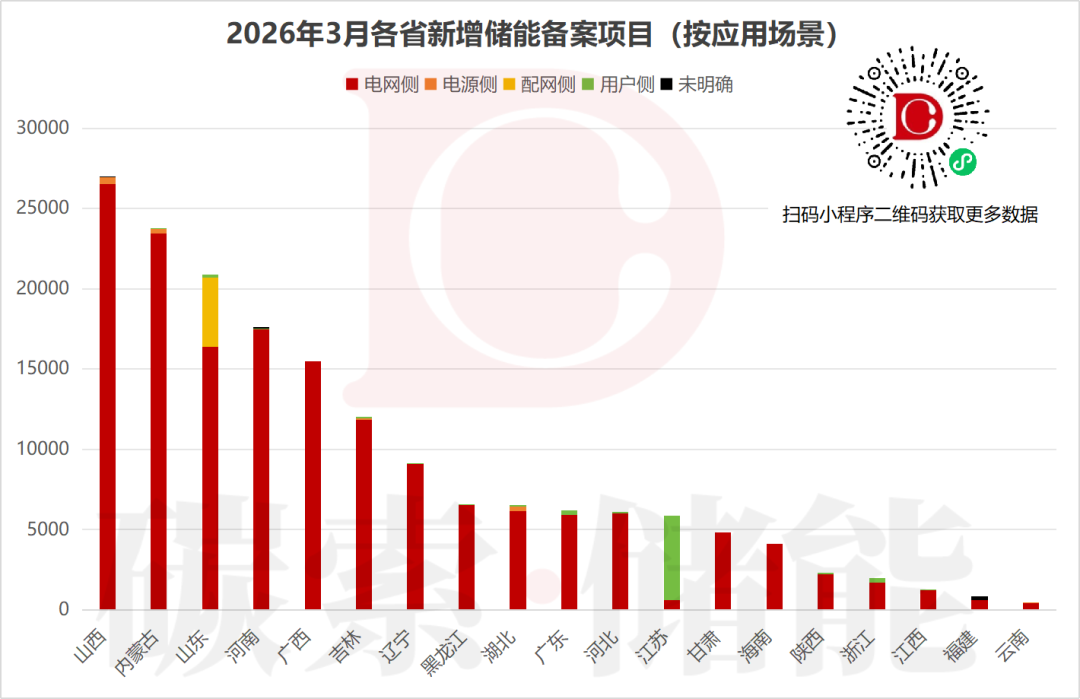

2. regional pattern: the three northern provinces lead the way, and the power grid side dominates

The regional concentration is significant. Shanxi (27.01GWh), Inner Mongolia (23.72GWh) and Shandong (20.90GWh) provinces accounted for nearly half of the total number of filings in the country, forming an obvious first echelon. From the application scenario, the grid side project occupies an absolute dominant position, especially in Shanxi, Inner Mongolia and other provinces accounted for more than 95%.

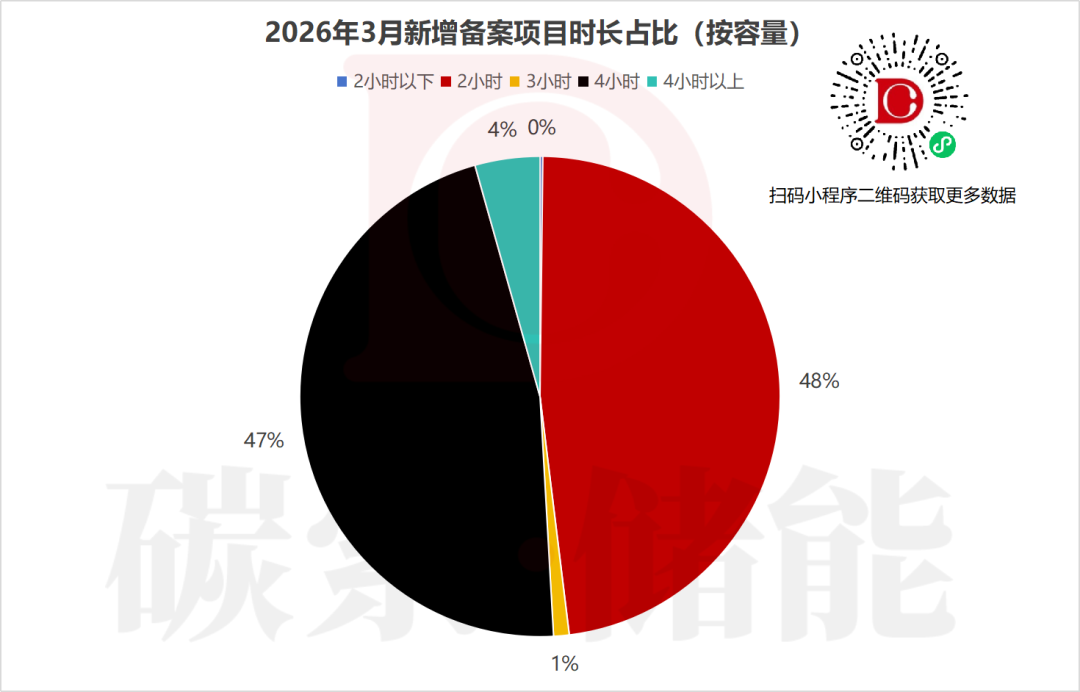

2-hour and 4-hour projects together account for more than 95%, dominating the market. It is worth noting that the previous pattern of 2 hours is changing, the proportion of long-term energy storage projects of 4 hours and above continues to rise, and the commercialization process exceeds expectations, reflecting the urgent need for long-term energy storage for new energy bases and grid peaking.

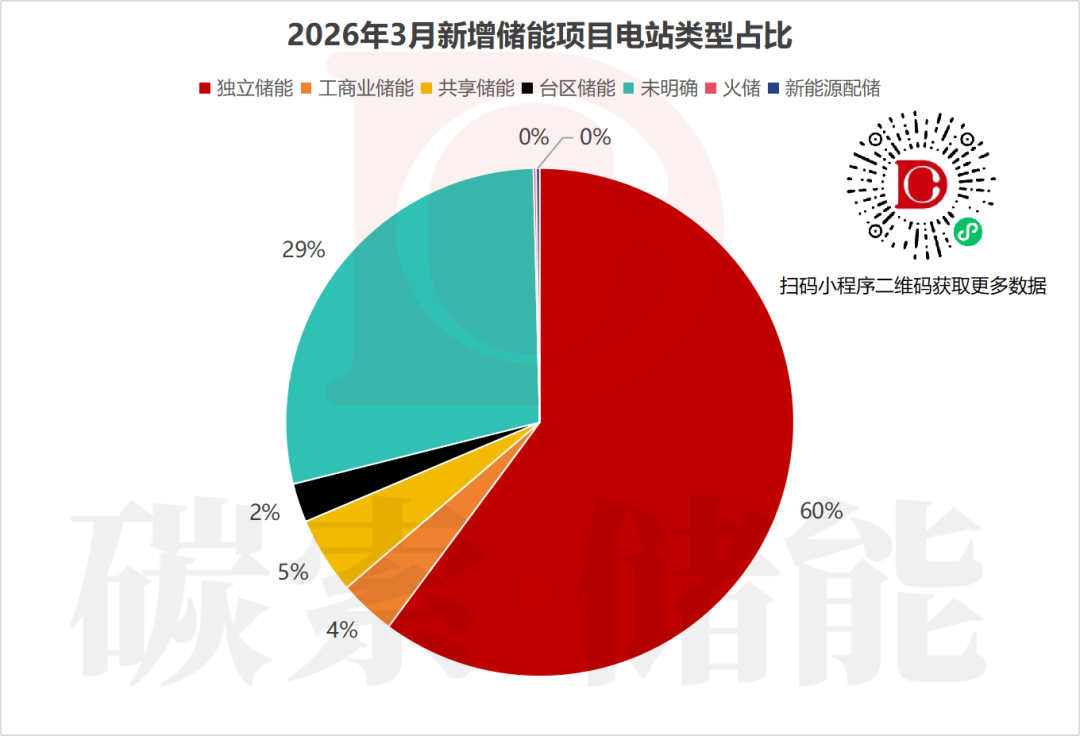

On the item type, independent energy storage has become the absolute main force with a proportion of about 60%. Its clear revenue model (capacity leasing, spot arbitrage, ancillary services) and policy support are the core drivers. Other types such as industrial and commercial energy storage and shared energy storage are small.

The market price competition is fierce, especially in the independent energy storage field. 0.7-1.3 yuan/Wh low-price range projects accounted for a total of 77%, becoming the absolute mainstream of the market. The price difference is mainly affected by the technical route, the price of lithium battery is low, the price of new technologies such as liquid flow battery and compressed air energy storage is high. Head enterprises by virtue of the scale advantage to lower the offer, the industry reshuffle pressure intensified.

There are 21 large projects over 1GWh filed in March, reflects the current trend:

Regional concentration: Inner Mongolia (9), Shandong (4), Jilin (2) project number leading.

technical diversity: the project is mainly based on independent energy storage with 4-hour configuration. at the same time, there are many long-term and new technology demonstration projects such as compressed air energy storage with 6-hour configuration and 5-hour liquid air energy storage.

Core demand matching: large-scale project configuration is concentrated in 2-6 hours, closely matching the core demand of grid side peak adjustment and new energy consumption.

the current market has entered a critical period of “structural upgrading”, with three major trends highlighted:

1. long-term acceleration: long-term energy storage of 4 hours and above has become the main force in large-scale projects, changing from “optional” to “just needed, drive the commercialization of non-lithium technologies such as compressed air energy storage and flow batteries.

2. Intensified centralization: The market is highly concentrated in the northern energy province and the independent energy storage scenario on the grid side. Regional differentiation is obvious, with large-scale new energy base areas become the main battlefield, the user side and other market segments have yet to be large-scale breakthrough.

3. The price war is heating up: low-price competition has become the mainstream strategy, and cost control ability has become the key to the survival of enterprises. The industry is facing a reshuffle and needs to find a balance between cost, technology and service quality.

For industry participants, it is necessary to seize the market opportunities brought about by independent energy storage and long-term energy storage, and to be alert to the quality risks that may be caused by low-price competition. As the weather gets warmer and construction conditions improve, a number of large-scale projects prepared in March will enter the construction stage one after another. The progress of the landing of nine GWh-level projects in Inner Mongolia, the cost trend of compressed air energy storage, the scale-up process of flow batteries, and the further landing of energy storage support policies in various regions are all worthy of continuous attention.

Only by finding a balance between cost control and technology upgrading, deeply cultivating subdivision scenarios and improving service quality, can we gain a firm foothold in the new round of industry competition and grasp the long-term development opportunities of the energy storage industry.

{kind=link}