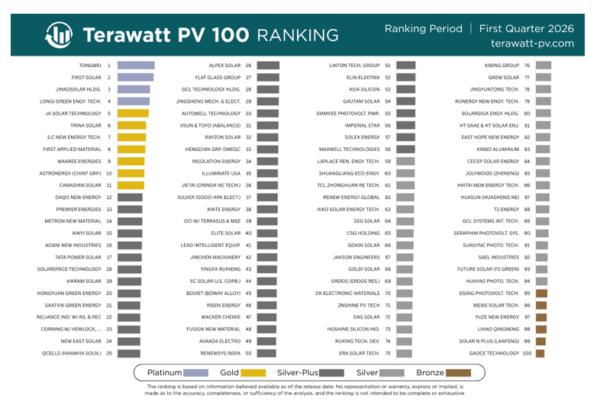

the latest Terawatt PV 100 list released by the Terawatt PV Research in the United States has for the first time established a comprehensive ranking and rating system covering the whole photovoltaic manufacturing ecology. in the list in the first quarter of 2026, tongwei ranked first in the world. this list not only ranks the top 100 enterprises, but also divides the echelons from platinum to copper, fully showing the current real pattern of global photovoltaic manufacturing. The list adopts a new evaluation method, which includes industrial chain enterprises from polysilicon to components, material suppliers from crucible to photovoltaic glass, and equipment manufacturers from crystal pulling furnace to string welding machine into the benchmarking scope. The comprehensive scores are based on the three core indicators of production capacity scale, financial strength and enterprise transparency, breaking the previous limitation that it is difficult for different track enterprises to compare horizontally.

Chinese enterprises account for nearly 60% of the TOP100, with only two non-Chinese enterprises in the top 10 list: First Solar and Waaree, jiejia Weichuang became the highest-ranked equipment supplier, while First Applied ranked first among materials companies. There are 21 companies headquartered in India in the TOP100 list, of which 12 are mainly engaged in raw material supply and 10 are focused on equipment manufacturing, showing a strong rise. The list finally assessed 4 platinum-grade enterprises, namely Tongwei, First Solar, Jingke, Longji, Jingao, Tianhe, Jiejia Weichuang, First Applied, Waaree, Chint and Artes Solar, which received gold-grade ratings.

the birth of the TOP100 list is essentially the inevitable result of the continuous deepening of the global photovoltaic supply chain review. At the beginning of the development of the industry, component procurement was mostly based on price and supply capacity. However, after the United States launched the “Solar I” double-reverse investigation on China’s crystalline silicon batteries in 2012, the industry rules began to change completely. Since then, the United States has successively introduced Solar II, Solar III and Solar IV series of tariff measures, gradually expanding its coverage from China to Southeast Asia and India, forcing purchasers to strictly check the origin of products. The UFLPA Act of 2022 further extends the supply chain traceability to polysilicon, superimposes the popularization of global ESG regulatory requirements, and upgrades the review of photovoltaic supply chain from regional policy to global consensus. The focus of the industry is no longer limited to the location of enterprise headquarters and ownership structure, but goes deep into the business model, technical route, GW-level production capacity, market share change, financial health and operation transparency. Fine verification of the whole industry chain has become the mainstream trend in the industry.

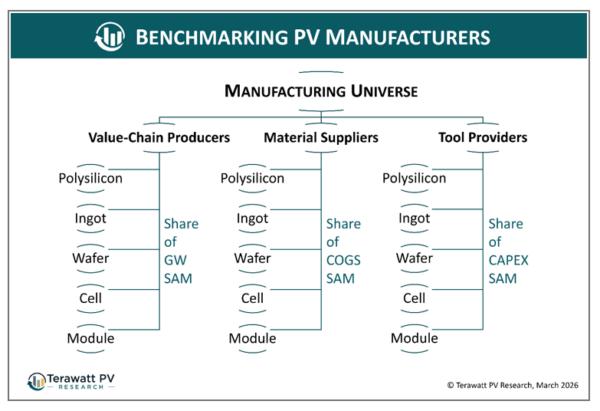

in order to realize the scientific benchmarking of all ecological enterprises, Terawatt PV 100 regards photovoltaic manufacturing as a unified overall market, differentiated capacity scoring standards are set for different types of enterprises. Component manufacturers are based on quarterly and annual GW capacity, material suppliers refer to the proportion of raw materials to sales costs, and equipment enterprises are calculated according to the capital expenditure of production lines. Scores of different business links can be calculated on top of each other. Enterprises with the layout of the whole industrial chain are more likely to obtain high scores. The higher the market share of a single subdivision track, the higher the capacity scale score. The financial evaluation link does not adopt a general model, but combines the characteristics of large cyclical fluctuations and concentrated product structure of the photovoltaic industry, selects the liquidity and debt indicators of more than 150 enterprises since 2020, taking into account both short-term and long-term operating data, and adds parent company credit support indicators for large groups such as Adani, Reliance and Tata, so that the score is more in line with the actual situation of the industry. Corporate transparency, as the third core dimension, focuses on ESG disclosure, supply chain traceability, equity structure clarity and information disclosure, in line with the trend of active and transparent operation of enterprises in the industry. The final score of the enterprise is weighted by three dimensions, and the minimum capacity threshold is set for all types of enterprises, and the rating is obtained through Z-value analysis, based on the complete data from 2020 to the first quarter of 2026, with strong dynamics, and the overall ranking and rating in the industry’s downward cycle can be adjusted simultaneously.

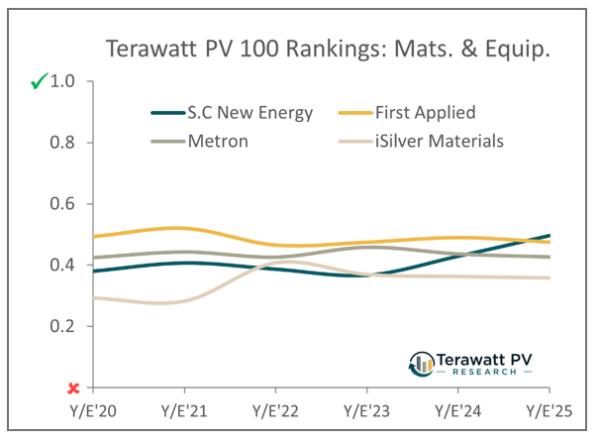

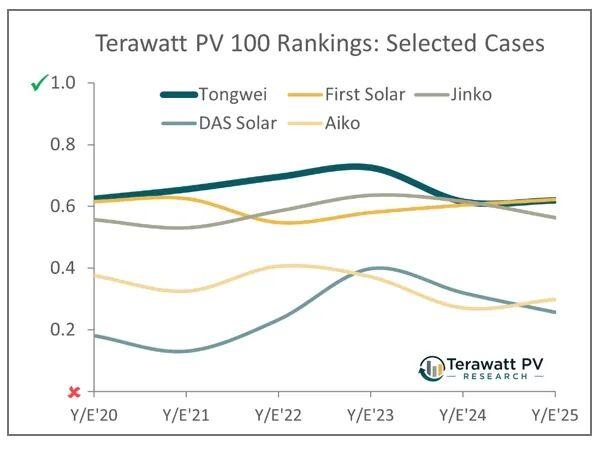

judging from the core characteristics of the list in the first quarter of 2026, the whole industry chain component manufacturers are still the main force of the list, polysilicon, silicon ingots, silicon chips, batteries and component head companies generally rank high, while leading companies in the materials and equipment track also perform well. Follett and Xinyi Glass are in the top 30, Meichang New Materials are in the TOP15, and Jiejia Weichuang and First Applied are in the top 10. Under the background of sharp price fluctuations in the industry in the past five years, the overall operational stability of materials and equipment companies is significantly better than that of downstream manufacturers. Tongwei and First Solar are firmly in the top two places on the list. Relying on the leading production capacity of polysilicon and battery links, Tongwei’s superposition component business continues to expand to the top of the list. At the same time, Tongwei obtains excellent transparency score with high information disclosure level. However, its comprehensive score continues to decline from 2023 onwards, with its short-term profit index falling by more than 50% from 2024 to 2025. First Solar has steadily improved its score since 2022, achieving full coverage and full value chain with thin film technology, financial strength and corporate transparency are at the top level of the industry, but also reflects the impact of this round of industry adjustment on Chinese enterprises is more concentrated.

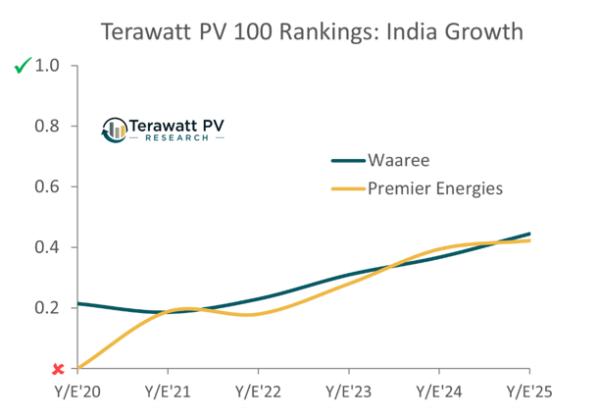

the batch entry of Indian enterprises has become the biggest highlight of this list. among the 21 enterprises on the list, there are not only large groups such as Adani, faithfulness and Tata, but also enterprises deeply engaged in photovoltaic field such as Waaree, Premier Energies and Vikram, as well as Alpex and Avaada relying on local market dividends, in the last 12 to 18 months of rapid expansion of components of the new manufacturers, Waaree and Premier Energies ranked the most significant compared to 2020.

As a highly dynamic industry list, terawatt PV 100 will also see a number of significant adjustments in 2026. In the second quarter list to be released in June, if some Chinese enterprises shut down production capacity, carry out asset disposal or debt restructuring in the first half of the year, the ranking of medium and low echelon enterprises may drop sharply. India’s photovoltaic industry is still expanding rapidly, and it is estimated that 5 to 10 enterprises with new production capacity of 2GW-5GW modules will be shortlisted in the next six months. At the same time, some photovoltaic equipment enterprises on the list this time rely on deferred revenue since 2023, the subsequent ranking will also change with the actual operating conditions, the global photovoltaic manufacturing pattern of a new round of reshuffle is continuing.

{kind=link}