N-type solar modules have emerged as the dominant choice in tenders during January and February in China, comprising over 70% of the market share. This shift has been accompanied by a substantial 51% drop in module prices over the past year.

The industry landscape has witnessed noteworthy signals as we step into 2024. Factors such as a slight uptick in polysilicon costs and lower production rates during China’s New Year holiday have prompted solar module manufacturers to hint at potential price rises.

This trend was validated in recent bids where n-type module prices have increased by CNY 0.03-0.04/W compared to pre-holiday rates.

However, with production resuming in March, the industry foresees a minor downward trend in supply chain prices.

Examining the tender data in January and February, p-type module prices fluctuated between CNY 0.85-0.92/W. Meanwhile, n-type bids displayed a broader range, varying from CNY 0.89-0.98 CNY/W, down about 50% year-on-year.

N-type dominance and shifting demand

In the first two months of 2024, over 67 GW of tenders have revealed results. About 8 GW was allocated to individual projects and the remaining 60 GW for framework procurement.

Key players like China Petroleum and China Resources exclusively chose n-type mono-bifacial modules in their tenders during this period.

Other tenders include PowerChina with over 70% of n-type tenders, China Southern Power Grid with about 60%, and China National Nuclear Corporation (CNNC) with about 25%, highlighting the increasing popularity of n-type products.

As for p-type modules, the market is experiencing a shift in demand towards higher-power modules, specifically those exceeding 570W/580W.

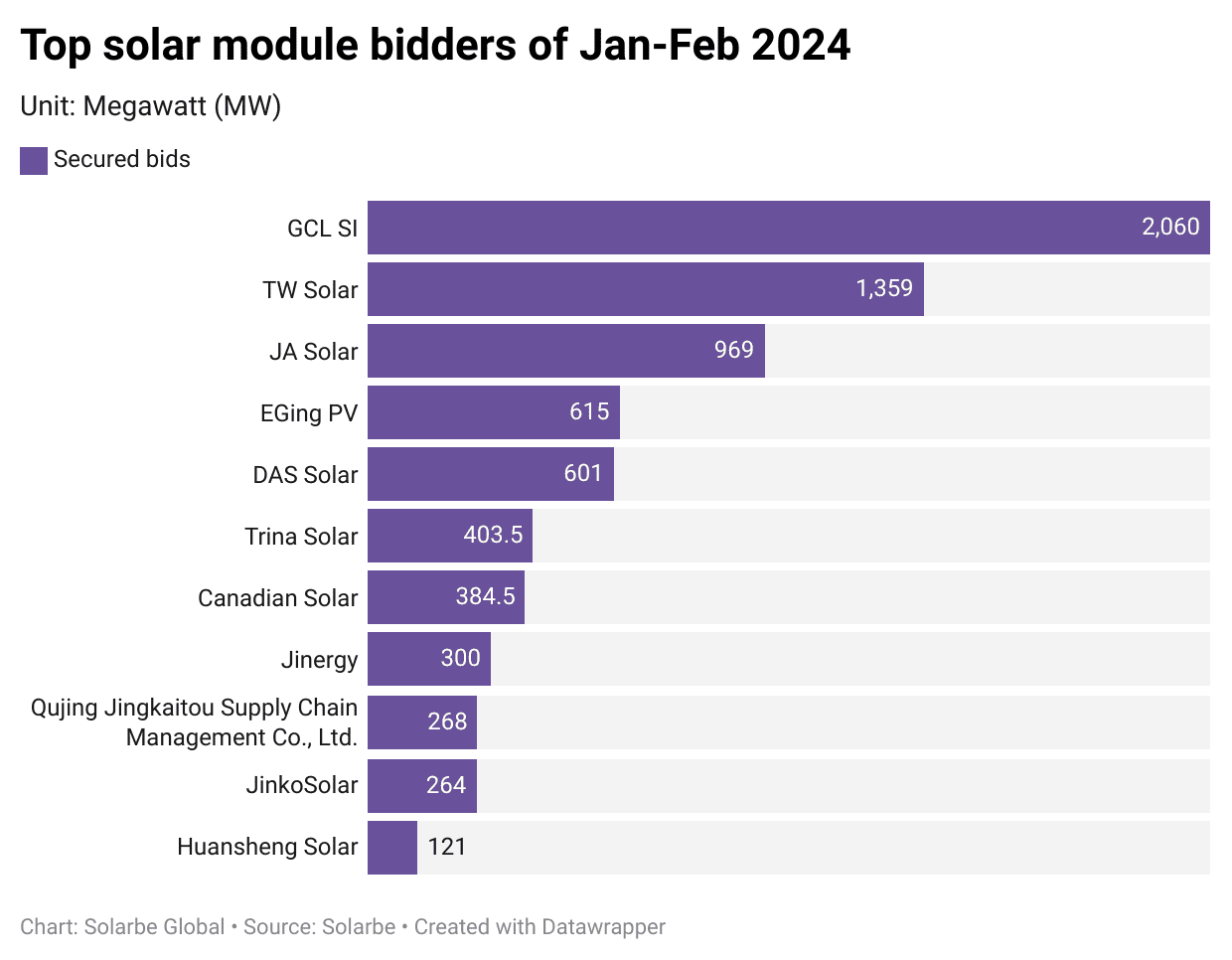

GCL SI, TW Solar stand out

GCL System Integration (GCL SI) led the market with 2 GW secured bids in the first two months of 2024. GCL SI told Solarbe that the company has shipped over 4 GW of modules in the fourth quarter of 2023, making it one of the world’s top 10 module suppliers by shipment volume in the past year.

TW Solar closely followed with 1.36 GW of secured tenders, including 1.17 GW from China Resources. Solarbe’s data shows that the company has shipped a total of 32 GW in 2023.

JA Solar claimed the third spot with about 970 MW. Other companies that secured bids include EGing PV, DAS Solar, Trina Solar, Canadian Solar, Jinergy, JinkoSolar, Huansheng Solar, etc.

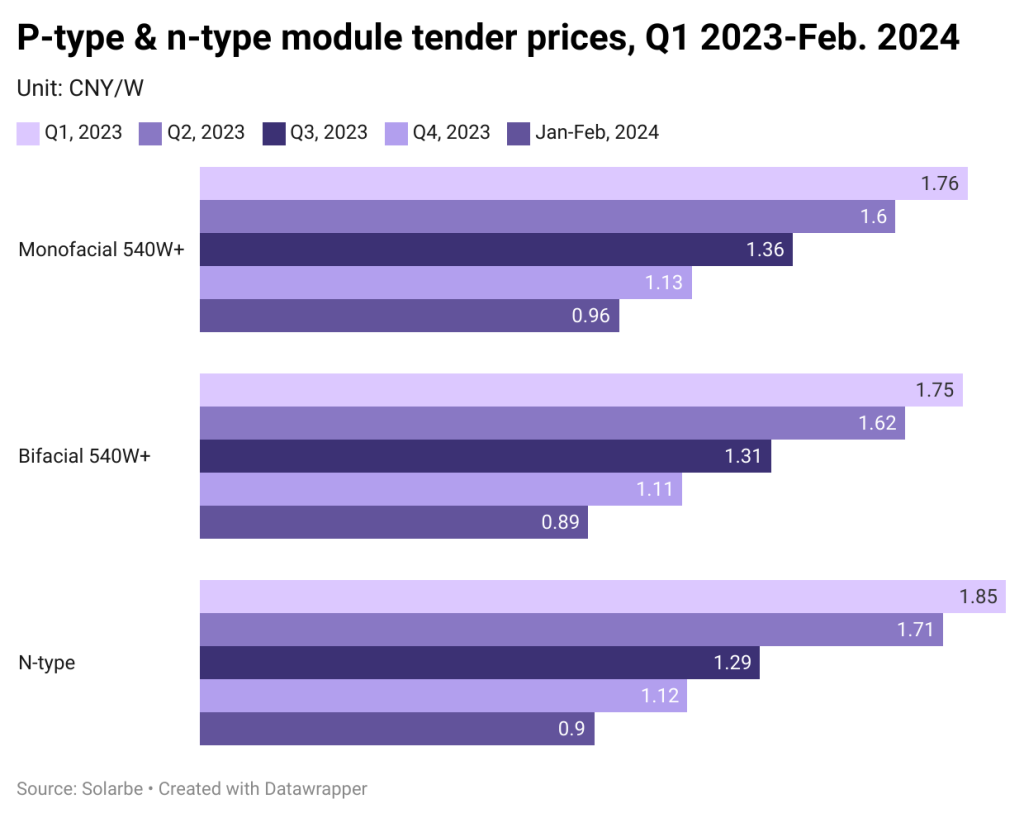

N-type prices down by 51%

Regarding bidding results for individual projects, the solar module prices have notably declined from Q1 2023 to the first two months of 2024. Specifically:

- Single-sided 540W+ modules saw the average bid price drop from CNY 1.761/W to CNY 0.96/W, marking a substantial 45% reduction.

- Bifacial 540W+ modules witnessed a drop from CNY 1.749/W to CNY 0.89/W during the same period, representing a 49% decrease.

- N-type module prices decreased from CNY 1.849/W to CNY 0.903/W, down by 51%.

According to Solarbe, some leading and emerging brands have explicitly shifted away from competing in the p-type market, focusing their efforts on the n-type market. This strategic move has led to intensified competition and substantial price reductions in n-type modules.

{kind=link}