The latest report commissioned by the German Machinery and Equipment Manufacturing Association (VDMA) shows that driven by global capacity expansion, the cumulative global market for photovoltaic manufacturing equipment will reach $250 billion to $300 billion in the next decade, with annual expenditures expected to increase from $16.6 billion in 2025 to $43.8 billion in 2035.

The report pointed out that although China controls more than 80% of the world’s silicon-based photovoltaic capacity, European equipment still has advantages in life and process stability. However, due to the lack of local large-scale manufacturing deployment, European manufacturers are facing severe challenges. Competitiveness is facing severe challenges.

the report entitled” European Photovoltaic Machinery and Equipment Research “(European Photovoltaics Machinery And Equipment Study) was jointly written by the Fraunhofer Institute for Solar Energy Systems (Fraunhofer ISE) and ISC Konstanz. The report predicts that as countries expand the scale of solar energy production, the annual capital expenditure of global photovoltaic manufacturing equipment will rise sharply from $16.6 billion in 2025 to $43.8 billion in 2035, thus pushing the total global cumulative market in the next decade to fall in the range of $250 billion to $300 billion.

At present, Asian competitors, led by China, continue to dominate the global photovoltaic manufacturing sector with high subsidies, controlling more than 80% of production capacity in all parts of the silicon-based value chain. The analysis shows that although competitors are outstanding in improving throughput and productivity, European equipment still maintains a leading position in terms of service life and process stability.

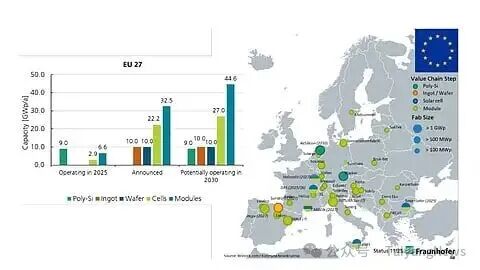

However, European equipment manufacturers lack strong local market support. Although several gigawatt-scale manufacturing projects have been announced, substantial investment remains limited. As of 2025, the EU will have an annual operating capacity of 9GW of polysilicon, 2.9GW of solar cells and 6.6GW of photovoltaic modules, with no ingot or wafer capacity. Based on public statements, the EU is expected to build 10GW of ingot and silicon wafer capacity, 22.2GW of battery capacity and 32.5GW of component capacity.

In an optimistic scenario, the authors of the report believe that by 2030, the EU’s polysilicon operating capacity will reach 9GW, ingots and silicon wafers will each reach 10GW, solar cells will reach 27GW, and photovoltaic modules will reach 44.6GW. Dr. Ralf Preu, Director of the Photovoltaic Department at Fraunhofer ISE, said: “Europe continues to develop efficient solar manufacturing technologies, but without large-scale industrial deployment at home, its competitiveness will be at stake. We have excellent research capabilities, and what we need now is a real factory with industrial excellence.”

The global PV market is expected to grow by about 2.5 times by 2035, with 1,650GW of new annual installed capacity. With the emergence of new technologies such as back contact (BC), heterojunction (HJT) and laminated cells, European manufacturing has ushered in new expansion opportunities. At present, Europe has deep experience in TOPCon, the mainstream technology in the industry. Dr. Radovan Kopecek, co-founder of ISC Konstanz, said: “European machinery has proven its strength in the current TOPCon technology. The technology transition to back contact, HJT and stacked cells has created significant opportunities for European equipment suppliers, but speed is of the essence, and customers are increasingly prioritizing short payback cycles, integrated solutions and fast response times.”

As competition intensifies outside China, countries such as India and the United States are emerging as new manufacturing markets, and the report authors make a number of recommendations for European companies, including expanding turnkey engineering (turnkey) capabilities, developing risk-sharing business models, strengthening after-sales service structures, and improving local presence in key markets. In addition, the report calls on industry and policymakers to take decisive action to coordinate industrial policy at the European level, including the provision of targeted investment support and procurement plans. In a September 2025 report, Fraunhofer ISE and SolarPower Europe recommended urgent policy support, including capital expenditure (CapEx), operating expenditure (OpEx) and output-based incentives, to close the gap between the EU and China in PV module manufacturing costs.

{kind=link}